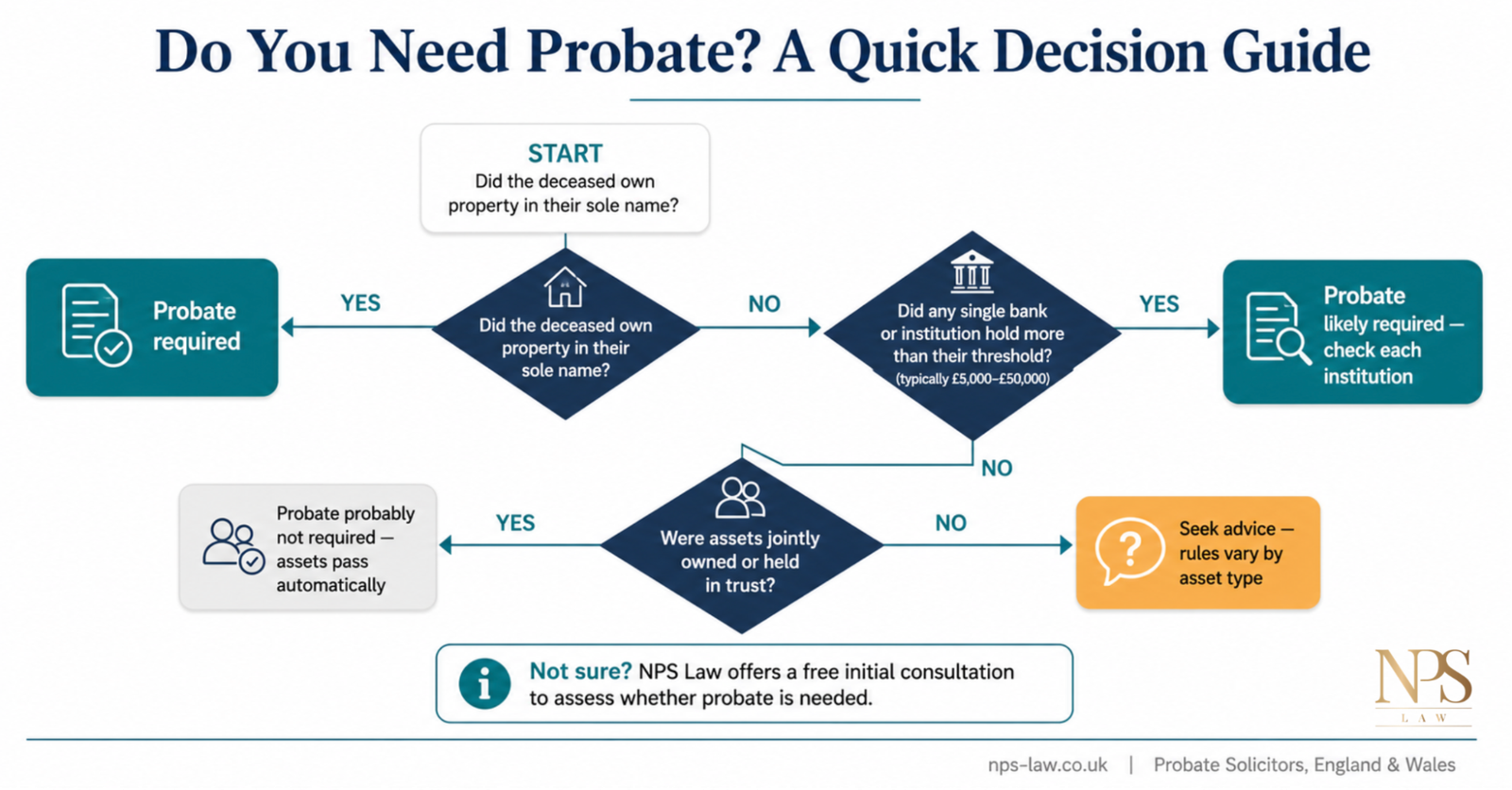

| • Probate is required when the deceased owned property in their sole name, or held assets above each bank’s individual threshold (typically between £5,000 and £50,000). |

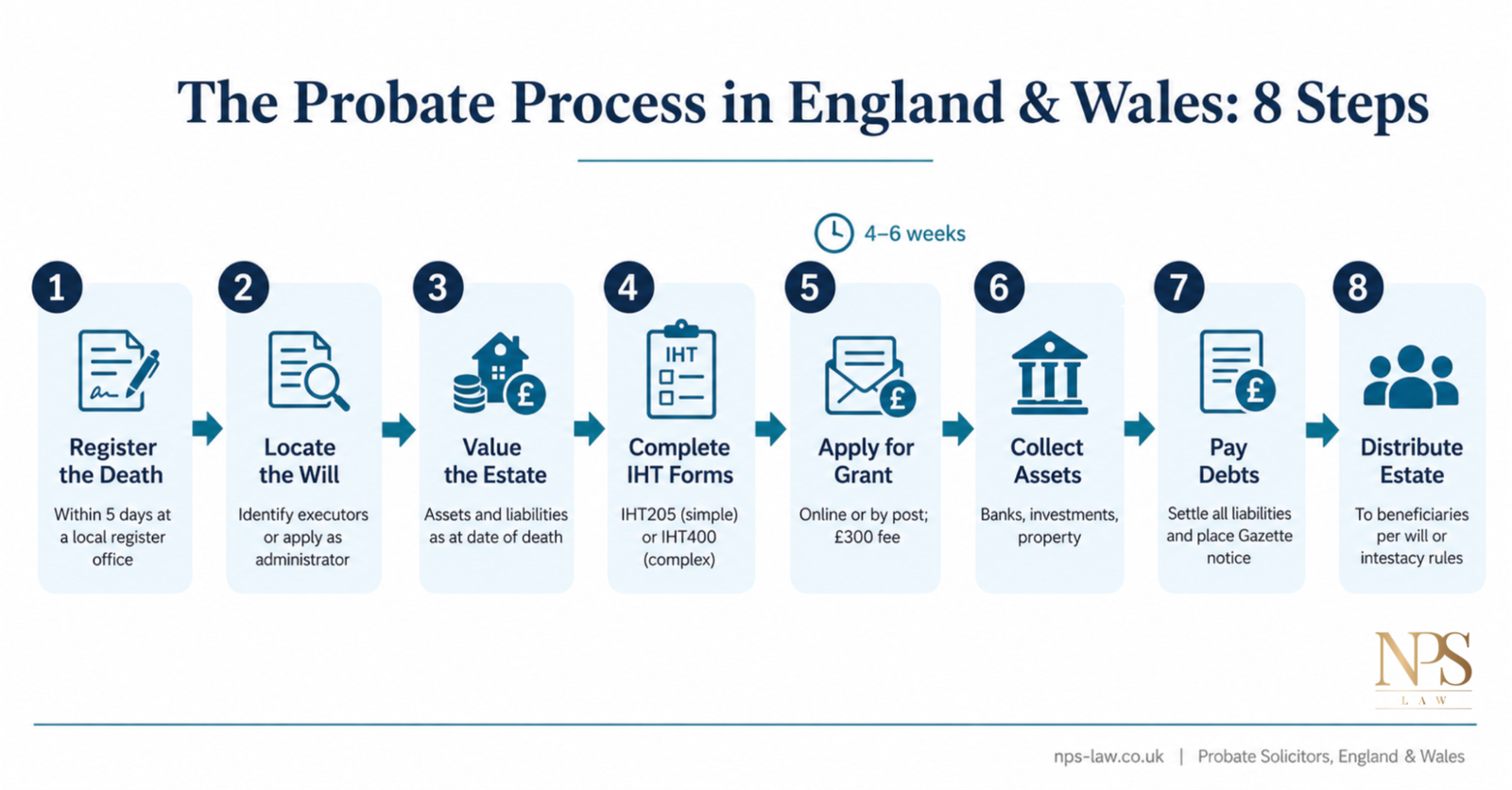

| • The process follows eight key steps, from registering the death to distributing the estate to beneficiaries. |

| • Applying for a Grant of Probate costs £300 in England and Wales; estates worth less than £5,000 are exempt from this fee. |

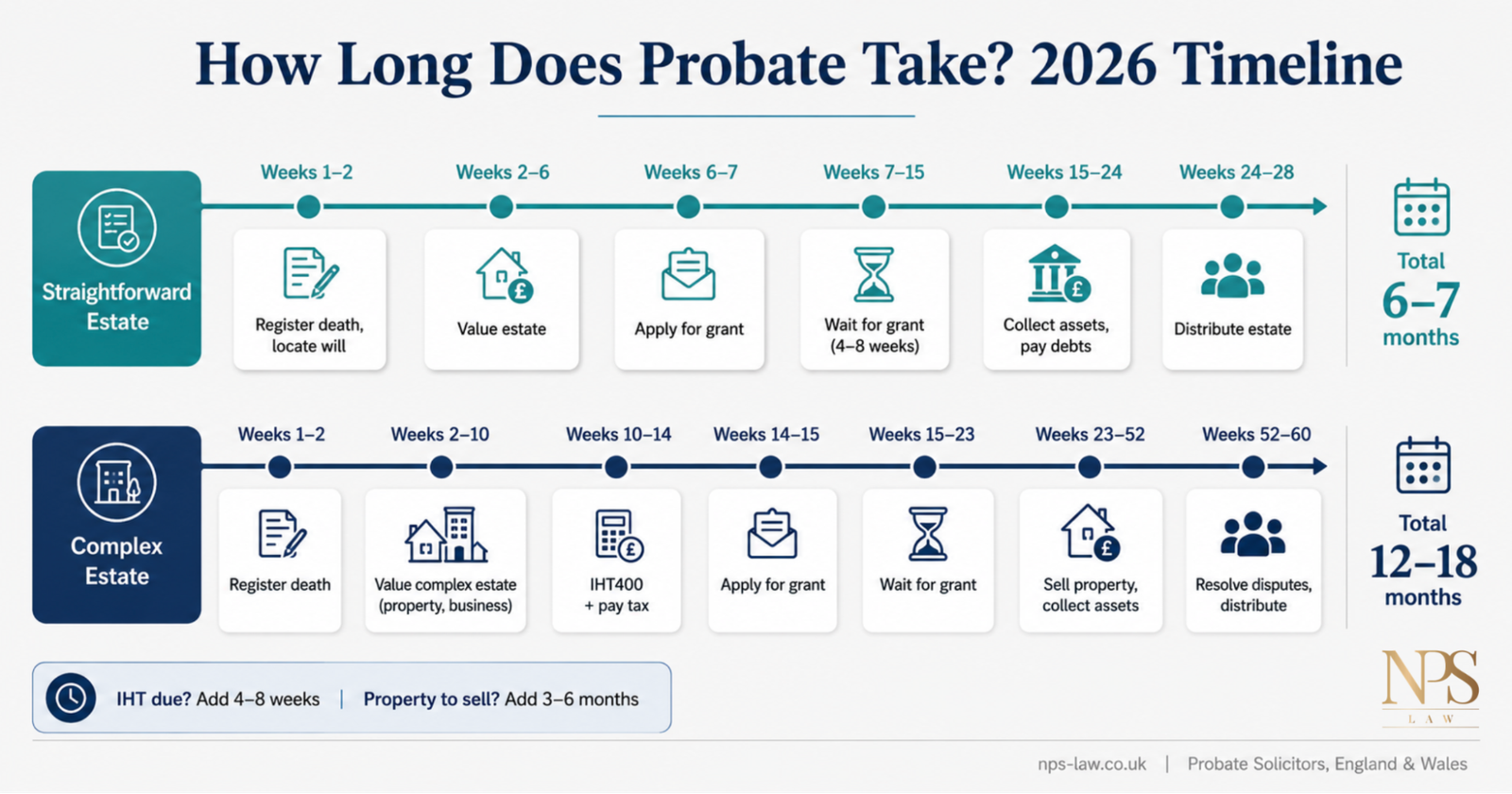

| • A straightforward estate typically takes 6 to 12 months from death to final distribution; complex estates can take 12 to 18 months or longer. |

| • A solicitor is not legally required, but is strongly recommended where the estate involves Inheritance Tax, disputed wills, overseas assets, or insolvent estates. |

When someone dies, their property, money and possessions do not automatically pass to their beneficiaries. In most cases, you will need to go through probate: the legal process of administering the deceased’s estate. This guide explains every step of the probate process in England and Wales in 2026, from registering the death to distributing assets to beneficiaries.

If you are new to probate and want to understand the basics before reading this guide, see our introduction: What Is Probate and How Does It Work in the UK?

Whether probate is required depends on what the deceased owned and the thresholds set by each financial institution holding their assets.

Not every estate needs to go through probate. The key factors are whether the deceased owned property solely, and how much money was held at each bank or financial institution.

| Bank / Institution | Approximate Probate Threshold |

|---|---|

| Barclays | £50,000 |

| Halifax / Bank of Scotland | £50,000 |

| HSBC | £50,000 |

| Lloyds Bank | £50,000 |

| NatWest / Royal Bank of Scotland | £15,000 |

| Santander | £50,000 |

| Nationwide Building Society | £30,000 |

| Virgin Money | £35,000 |

| NS&I (National Savings) | £5,000 per product |

| Note | Thresholds change regularly. Always contact the institution directly to confirm. |

Executors named in the will apply for a Grant of Probate; where there is no will, an eligible person applies for Letters of Administration as an administrator of the estate.

The type of application you make depends on whether the deceased left a valid will.

The will names one or more executors. These are the people with the legal right to apply for probate. If you are named as executor, you are not legally required to take on the role. You may renounce (give it up permanently), or reserve your power to act at a later stage.

Where no valid will exists, the estate is administered under intestacy rules. An eligible person must apply for Letters of Administration. The priority order for who may apply is:

The death must be registered within five days at a local register office; you will need multiple certified copies of the death certificate.

Registering the death is the first practical step and must normally be completed within five days in England and Wales. Register at the register office nearest to where the death occurred.

What you will need: the medical certificate of cause of death, plus the deceased’s birth certificate, marriage certificate and NHS medical card if available.

How many death certificates to order: you will need one original certified copy for each institution holding assets (bank accounts, investments, insurance policies). Order at least 4 to 5 copies at the time of registration (£11 each); ordering additional copies later is more expensive and slower.

Tell Us Once: If the deceased lived in England or Wales, use the government’s Tell Us Once service (gov.uk) to notify HMRC, DWP, DVLA and the local council in a single step.

The original will must be submitted to the Probate Registry; a photocopy is not accepted under any circumstances.

Begin searching for the will in the first week after the death. The will may contain funeral wishes that need to be acted on promptly.

Where to look: the deceased’s home (desk, filing cabinet, safe), their solicitor, their bank’s safe deposit box, or the National Will Register (nationalwillregister.co.uk, fee applies).

If no will is found: the estate is distributed under intestacy rules. The person who applies for Letters of Administration becomes the administrator.

If the executor named in the will cannot act: any beneficiary of the estate may apply to the Probate Registry to act as administrator instead.

All assets and liabilities must be valued as at the date of death, not at the current date, and supported by written evidence from banks and valuers.

Producing an accurate estate valuation is critical for both the Inheritance Tax (IHT) calculation and the probate application. Assets must be valued at the date of death.

Because property values vary significantly across England and Wales, whether Inheritance Tax (IHT) is likely depends heavily on where the deceased lived. The table below shows average property values and approximate IHT exposure by region, to help executors assess whether the full IHT400 form will be required.

| Region | Average Property Value (2026 est.) | IHT Likely? |

|---|---|---|

| London | ~£540,000 | High (property alone may exceed threshold) |

| South East | ~£390,000 | Moderate to High |

| East of England | ~£340,000 | Moderate |

| South West | ~£310,000 | Moderate |

| East Midlands | ~£240,000 | Low to Moderate |

| West Midlands | ~£240,000 | Low to Moderate |

| Yorkshire & Humber | ~£210,000 | Low |

| North West | ~£210,000 | Low |

| North East | ~£165,000 | Very Low |

| Wales | ~£205,000 | Low |

Source: UK House Price Index estimates. IHT nil-rate band: £325,000 (basic). Residence nil-rate band adds up to £175,000 when a home passes to direct descendants.

https://www.gov.uk/government/statistics/uk-house-price-index-for-march-2026/uk-house-price-index-summary-march-2026

Even where no Inheritance Tax is due, HMRC forms must be completed and submitted before a Grant of Probate can be issued.

Inheritance Tax (IHT) is charged at 40% on the value of an estate above the nil-rate band of £325,000. If the deceased left their home to direct descendants, an additional residence nil-rate band of up to £175,000 may apply, giving a combined threshold of up to £500,000.

| Form | When to use it |

|---|---|

| IHT205 (or IHT400 — excepted estate route) | Estate is below £325,000 with no complex assets. No IHT due. Simpler form; submitted directly to the Probate Registry as part of the probate application. |

| IHT400 (full return) | Estate exceeds the IHT threshold; estate is above £3 million even if no tax is due; deceased made significant gifts in the last 7 years; or complex assets (business property, overseas assets, trusts) are involved. |

A common difficulty is that IHT must be paid (or arrangements made to pay it) before the Grant of Probate is issued, but the grant is needed to access the deceased’s assets. There are four practical solutions:

Applications can be made online or by post using form PA1P (where there is a will) or form PA1A (where there is no will); the current application fee is £300.

Once the estate has been valued and any IHT forms submitted, you can apply to the Probate Registry for the grant.

| Method | Details |

|---|---|

| Online (apply.probate.service.gov.uk | Available if the deceased lived in England, Wales or Northern Ireland. Typically processed in 4 to 6 weeks. Faster and less likely to result in queries. |

| By post (PA1P or PA1A form) | Use PA1P if there is a will; PA1A if there is no will. Send to: HMCTS Probate, PO Box 12625, Harlow, CM20 9QE. Typically processed in 6 to 8 weeks. |

For a full breakdown of probate fees and what affects the total cost, see: How Much Does Probate Cost in the UK? Solicitor Fees Explained [link:https://www.nps-law.co.uk/how-much-does-probate-cost-in-the-uk-solicitor-fees-explained-2026/]

Once the grant is issued, the executor has legal authority to access bank accounts, collect investments, and arrange the sale or transfer of property.

With the Grant of Probate or Letters of Administration in hand, you can now formally collect all the estate’s assets. Open a dedicated executor account at a bank to hold estate funds separately from your personal money.

If the estate includes property: selling a property typically adds 3 to 6 months to the probate process. Consider whether beneficiaries wish to buy the property before listing it on the open market. For guidance on property specifically, see: Can You Sell a House Before Probate Is Granted in the UK?

All debts must be settled before distributing the estate; placing a statutory notice in the London Gazette protects the executor from personal liability to creditors who were unknown at the time of distribution.

Before distributing anything to beneficiaries, all the deceased’s debts must be paid. If you distribute assets before settling debts, you may be personally liable to creditors.

Placing a statutory notice in the London Gazette, and where appropriate a local newspaper, protects executors from personal liability if unknown creditors emerge after distribution. The notice must run for at least two months before the estate is distributed. This step is not legally mandatory but is strongly recommended by solicitors and is standard professional practice.

Distribution should begin only after all debts are settled, the two-month statutory notice period has expired, and estate accounts have been prepared and approved by beneficiaries.

Once all debts are paid and the notice period has run, you can distribute the estate. Ask each beneficiary to sign a written receipt confirming what they have received.

For everything that happens after the grant is issued, see: Once Probate Has Been Granted, What Happens Next? link: https://www.nps-law.co.uk/how-much-does-probate-cost-in-the-uk-solicitor-fees-explained-2026/

A straightforward estate typically takes 6 to 9 months from death to final distribution; complex estates involving property sales, Inheritance Tax or disputes commonly take 12 to 18 months.

| Stage | Straightforward Estate | Complex Estate |

|---|---|---|

| Register death, locate will | Weeks 1 to 2 | Weeks 1 to 2 |

| Value the estate | Weeks 2 to 6 | Weeks 2 to 10 |

| Complete IHT forms | Weeks 4 to 6 | Weeks 8 to 14 |

| Apply for grant | Week 6 to 7 | Weeks 14 to 15 |

| Wait for grant to be issued | Weeks 7 to 15 (4 to 8 weeks) | Weeks 15 to 23 (6 to 8 weeks) |

| Collect assets, pay debts | Weeks 15 to 24 | Weeks 23 to 52 |

| Distribute estate | Weeks 24 to 28 | Weeks 52 to 60 |

| Typical total | 6 to 7 months | 12 to 18 months |

What extends the timeline: property sales typically add 3 to 6 months. IHT due adds 4 to 8 weeks. Overseas assets, business interests, or missing beneficiaries can each add several months. Probate Registry delays currently average 6 to 12 weeks for grant processing.

Processing times at the Probate Registry are broadly consistent across England and Wales for online applications. However, postal applications processed through probate registries in London and the South East may experience slightly longer queues during peak periods (January to March).

| Application type | Typical grant waiting time (2026) |

|---|---|

| Online application (all regions) | 4 to 6 weeks |

| Postal application (London and South East) | 7 to 10 weeks |

| Postal application (rest of England and Wales) | 6 to 8 weeks |

| Applications requiring follow-up queries | Add 4 to 8 weeks |

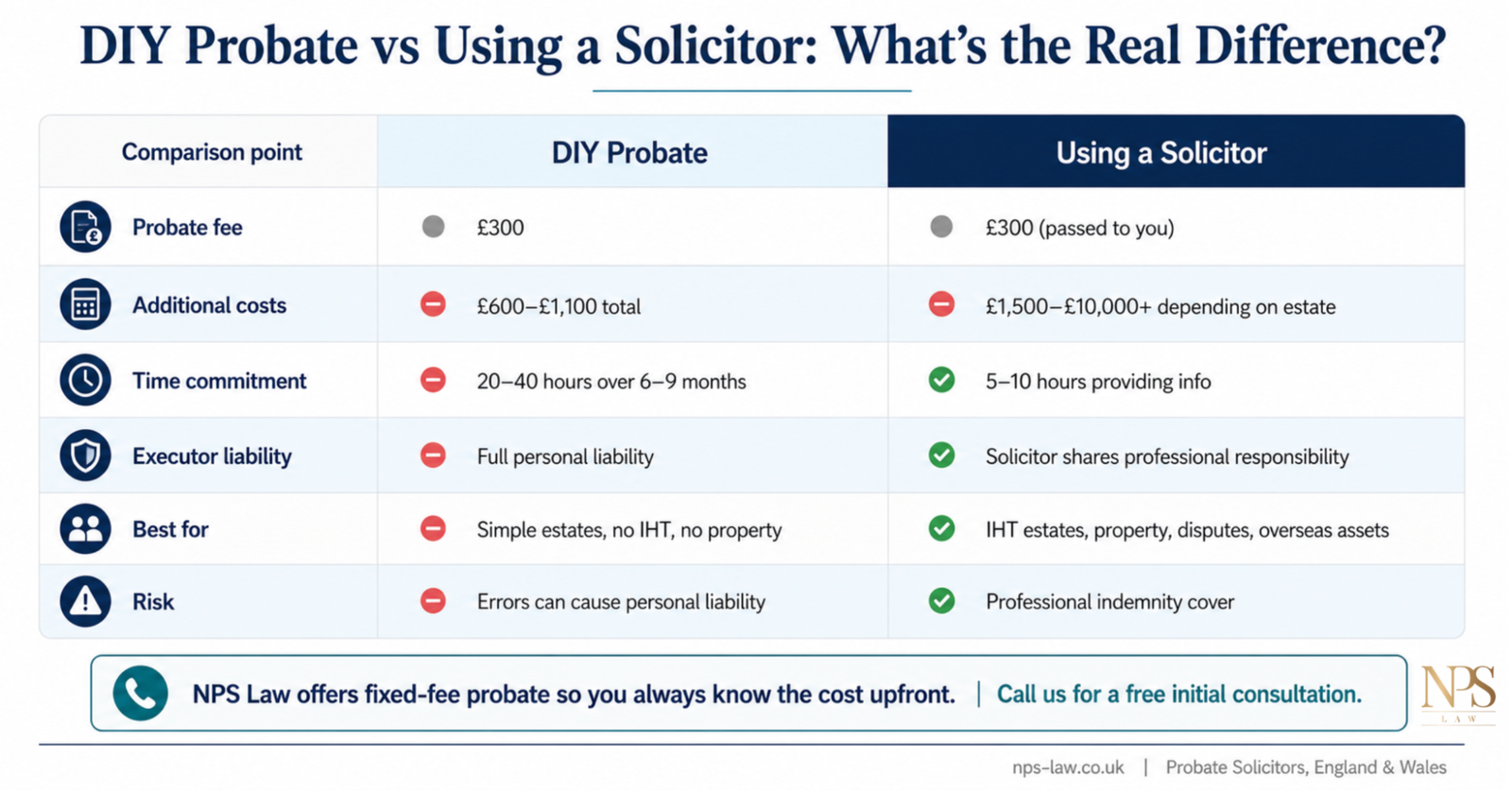

DIY probate costs between £300 and £1,000 in direct fees; instructing a solicitor typically costs between 1% and 3% of the estate value, or a fixed fee for straightforward estates

| Cost item | Amount |

|---|---|

| Probate application fee | £300 (estates over £5,000) |

| Death certificates (4 to 5 copies) | £44 to £55 |

| Extra certified copies of the grant | £1.50 each (order 5) |

| Property valuation (estate agent) | Free to £300 (RICS surveyor) |

| London Gazette notice | Approx. £200 to £300 |

| Postage and administration | £50 to £150 |

| Typical DIY total | £600 to £1,100 |

Using a solicitor: fixed-fee probate services typically start from £1,500 for straightforward estates. Hourly-rate or percentage-based fees can range from 1% to 3% of the estate value. NPS Law provides clear, fixed-fee probate services so you know the cost from the outset.

Need help with probate? Contact NPS Law for a free initial consultation. We offer clear, fixed-fee probate services across England and Wales.

A solicitor is not legally required for probate, but professional advice is strongly recommended when the estate involves Inheritance Tax, disputed wills, overseas assets, or when executors are uncertain about their duties.

Many people successfully complete probate without professional help, particularly for straightforward estates with no IHT, no property to sell, and no disputes. However, certain circumstances make it advisable to instruct a solicitor.

| Your situation includes... | Recommendation |

|---|---|

| The estate is above the £325,000 Inheritance Tax threshold | Consider a solicitor |

| The deceased owned property solely, or as tenants in common | Consider a solicitor |

| The validity of the will is in dispute | Consider a solicitor |

| A beneficiary or creditor has made a claim against the estate | Consider a solicitor |

| The estate includes overseas assets or foreign property | Consider a solicitor |

| The deceased had business interests or shares in a private company | Consider a solicitor |

| One or more beneficiaries cannot be traced | Consider a solicitor |

| The estate may be insolvent (debts exceed assets) | Consider a solicitor |

If any of the above apply to your situation, speak to a solicitor before proceeding. Contact NPS Law today for clear, practical advice on your next steps.

Once you have applied, the Probate Registry typically takes 4 to 6 weeks to issue the grant for online applications, and 6 to 8 weeks for postal applications. Applications that require follow-up queries or additional documents can take considerably longer. The time to complete the full probate process, from death to final distribution, is usually 6 to 12 months for a straightforward estate.

Yes. There is no legal requirement to instruct a solicitor for probate in England and Wales. Many executors successfully manage straightforward estates without professional help. However, if the estate involves Inheritance Tax, property, disputes, or overseas assets, professional advice is strongly recommended. Executors are personally liable for errors made during administration.

A Grant of Probate is issued when the deceased left a valid will and the executor named in that will is applying. Letters of Administration are issued where there is no will (intestacy), or where the named executor is unable or unwilling to act. Both documents grant the same legal authority to administer the estate.

If there is no will, you may still need to apply for Letters of Administration in order to access and distribute the estate. The process is broadly the same as applying for probate, but the estate is distributed according to the intestacy rules rather than the wishes of the deceased.

If an executor named in the will cannot be found, refuses the role, or lacks mental capacity, they may formally renounce their right to act. A beneficiary of the estate can then apply to the Probate Registry to act as administrator instead. If all named executors renounce, the estate is administered as if there were no executor.

All references verified June 2026.

©️ Copyright 2026 NPS Law is a trading name for NPS Law LLP. Solicitors of England and Wales. Authorised and Regulated by the Solicitors Regulation Authority. SRA Number 570169. A list of all Partners is available on the SRA directory for this firm. website designed by origin-media