When someone close to you dies, the last thing you want to think about is paperwork. Yet in most cases, the people left behind must deal with a legal process called probate before any of the deceased’s money, property or possessions can be distributed. For many families, this is completely unfamiliar territory.

This guide explains what probate means in plain English, walks through every stage of the process, sets out how long each stage typically takes, and highlights the key differences that apply depending on where in England the estate is located and the ages of those involved.

If at any point you would prefer to speak to a solicitor rather than read further, the NPS Law probate team is available to guide you through every step.

Need help with probate? Speak to an NPS Law solicitor today. Call us or use our online enquiry form for a free initial conversation.

Probate is the legal process of administering the estate of someone who has died. It covers everything involved in dealing with their money, property and possessions: valuing the assets, paying any taxes and debts, and ultimately passing what remains to the people entitled to inherit.

The word itself comes from the Latin probare, meaning to prove. In practice, it refers to the court process of proving that a will is valid and authorising someone to act on behalf of the estate.

Grant of Probate is the document issued when the deceased left a valid will. It confirms that the named executor has the legal authority to deal with the estate. You can find out more about NPS Law’s probate and estate administration services including how we support executors from application through to distribution.

Letters of Administration is the equivalent document issued when there is no will, or when the will did not name a living executor. It appoints someone (usually the next of kin) to act as administrator.

The practical effect is the same in both cases: the document unlocks the deceased’s assets and allows the estate to be settled.

This guide focuses on England and Wales. Scotland operates a separate system called Confirmation, administered through the Sheriff Court rather than the Probate Registry. Northern Ireland has its own Probate Office in Belfast. If the deceased held assets in more than one jurisdiction, you may need to obtain authority in each.

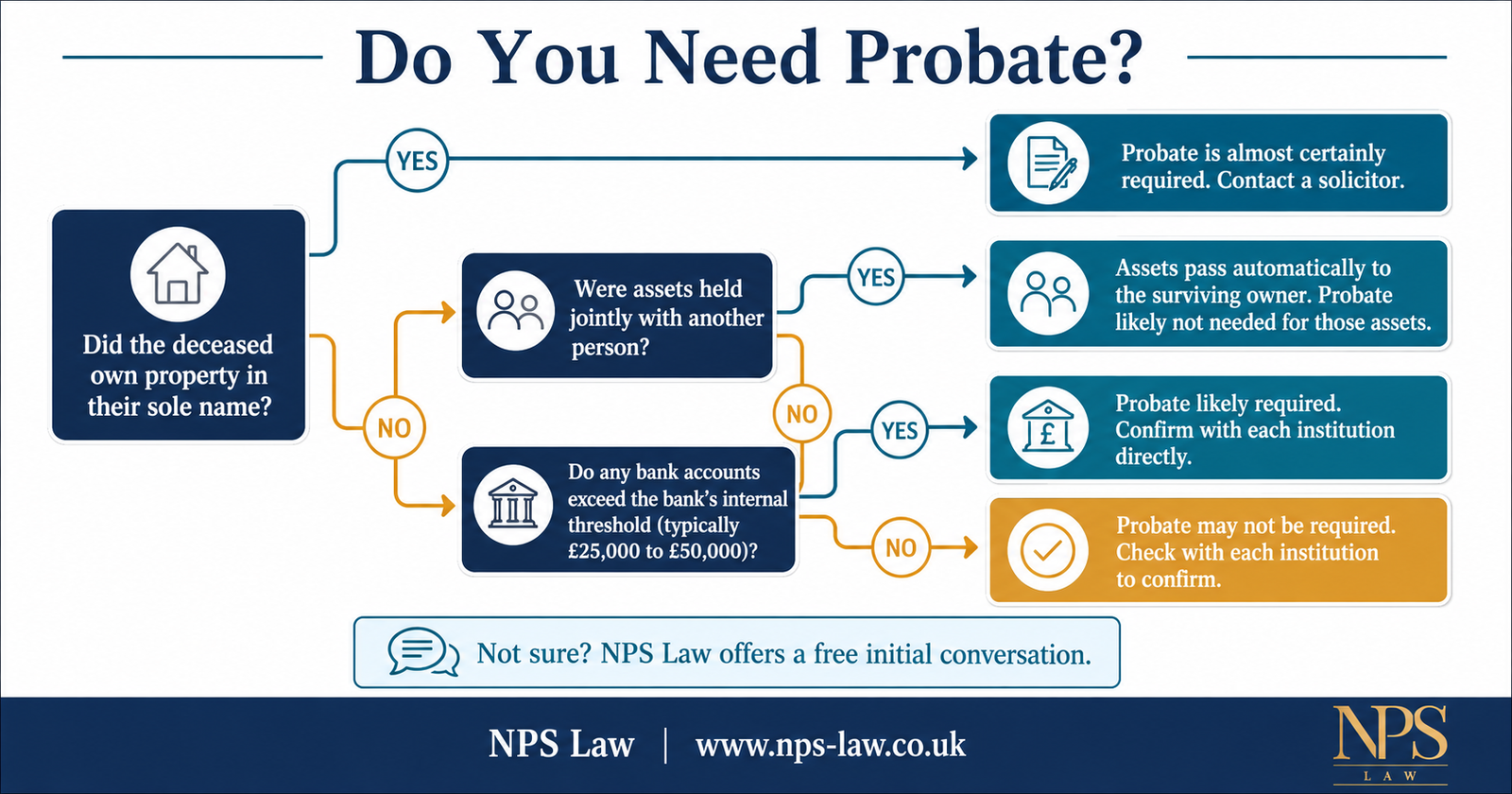

There is no single legal threshold that automatically triggers probate. Instead, it depends on the nature of the assets and the policies of the financial institutions holding them.

Banks and building societies each set their own limits. These figures are indicative and subject to change; always confirm directly with the institution.

| Institution | Approximate Probate Threshold | Notes |

|---|---|---|

| Barclays | Up to £50,000 | May release funds for funeral costs below threshold |

| HSBC | Up to £50,000 | Threshold applies per account |

| Lloyds / Halifax | Up to £50,000 | Joint accounts pass automatically |

| NatWest / RBS | Up to £25,000 | Lower threshold; confirm at branch |

| Nationwide | Up to £30,000 | Building society accounts may differ |

| Santander | Up to £50,000 | Subject to individual review |

| NS&I (Premium Bonds) | Up to £5,000 | Strict threshold; probate often needed above this |

If the deceased held accounts at multiple banks, each institution applies its own threshold independently. A solicitor can contact them on your behalf to confirm what is needed before you begin the application.

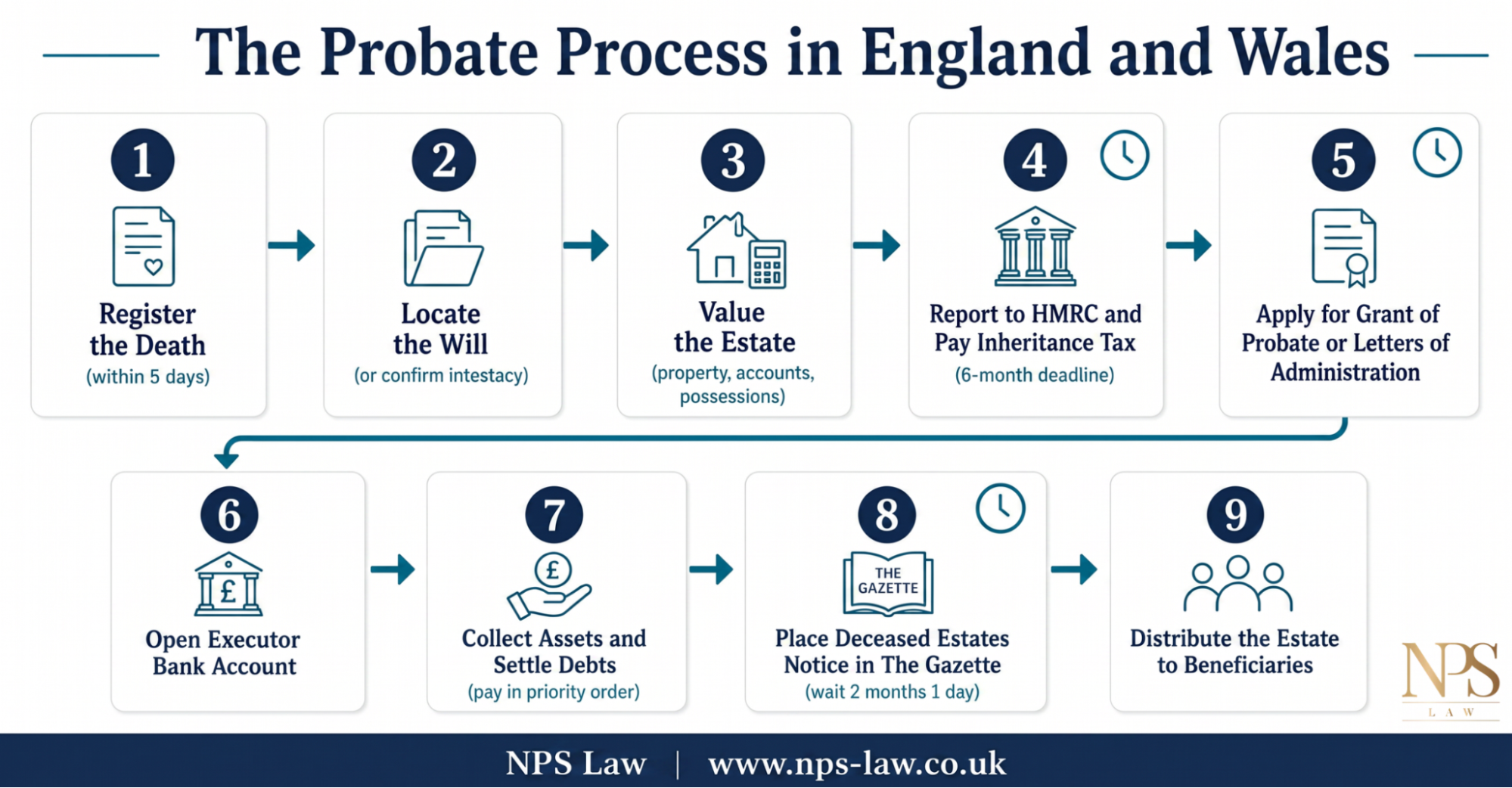

Every estate is different, but the process follows a consistent sequence. Below is a full walkthrough of each stage.

The death must be registered at the local register office within 5 days in England and Wales. You will need either a medical certificate from a doctor or permission from the coroner. Once registered, you receive the death certificate. Order several certified copies at the time since banks and other institutions will each require one.

Check the deceased’s home, any solicitor they used, and their bank’s safe deposit facility. If you cannot find the will, the National Will Register and local Law Society branches can help trace it. Make sure you have the most recent version: an earlier will may have been superseded.

If no will exists, the estate is described as intestate and the rules of intestacy determine who inherits and who can apply to administer the estate.

You need a full picture of what the deceased owned and owed on the date they died. HMRC expects the executor to look back over the previous seven years for gifts that may be subject to inheritance tax.

Inheritance tax (IHT) must be paid within six months of the end of the month in which the person died. For estates above the nil-rate band (currently £325,000, or up to £500,000 with the residence nil-rate band), IHT is charged at 40% on the value above the threshold.

Most executors use the Direct Payment Scheme, asking banks to release funds from the deceased’s accounts directly to HMRC before probate is granted. This avoids the executor needing to fund the tax personally.

Applications can be made online through the HMCTS Probate Service or by post using form PA1P (where there is a will) or PA1A (where there is no will). You will need to submit the original will, the death certificate, and confirmation that IHT has been reported.

The court fee is currently £300 for estates valued above £5,000. Additional certified copies cost £1.50 each and are worth ordering in quantity since multiple institutions will ask for them.

Once the grant is issued, open a dedicated executor bank account to collect the estate’s funds. Pay debts in the following order:

It is strongly advisable to place a Deceased Estates Notice in The Gazette (and a local newspaper) after receiving the grant. This invites any unknown creditors to come forward. Creditors then have two months and one day to make a claim. Distributing the estate before this window closes leaves the executor personally liable for any claims that subsequently arise.

Once all debts, taxes and expenses have been paid, prepare final estate accounts summarising the assets, liabilities and distribution. Send a copy to each main beneficiary and ask them to sign and return it. You can then distribute the estate according to the will, or according to the rules of intestacy if there is none.

It is sensible to wait at least ten months after applying for probate before making final distributions, to allow time for any Inheritance Act claims to be brought.

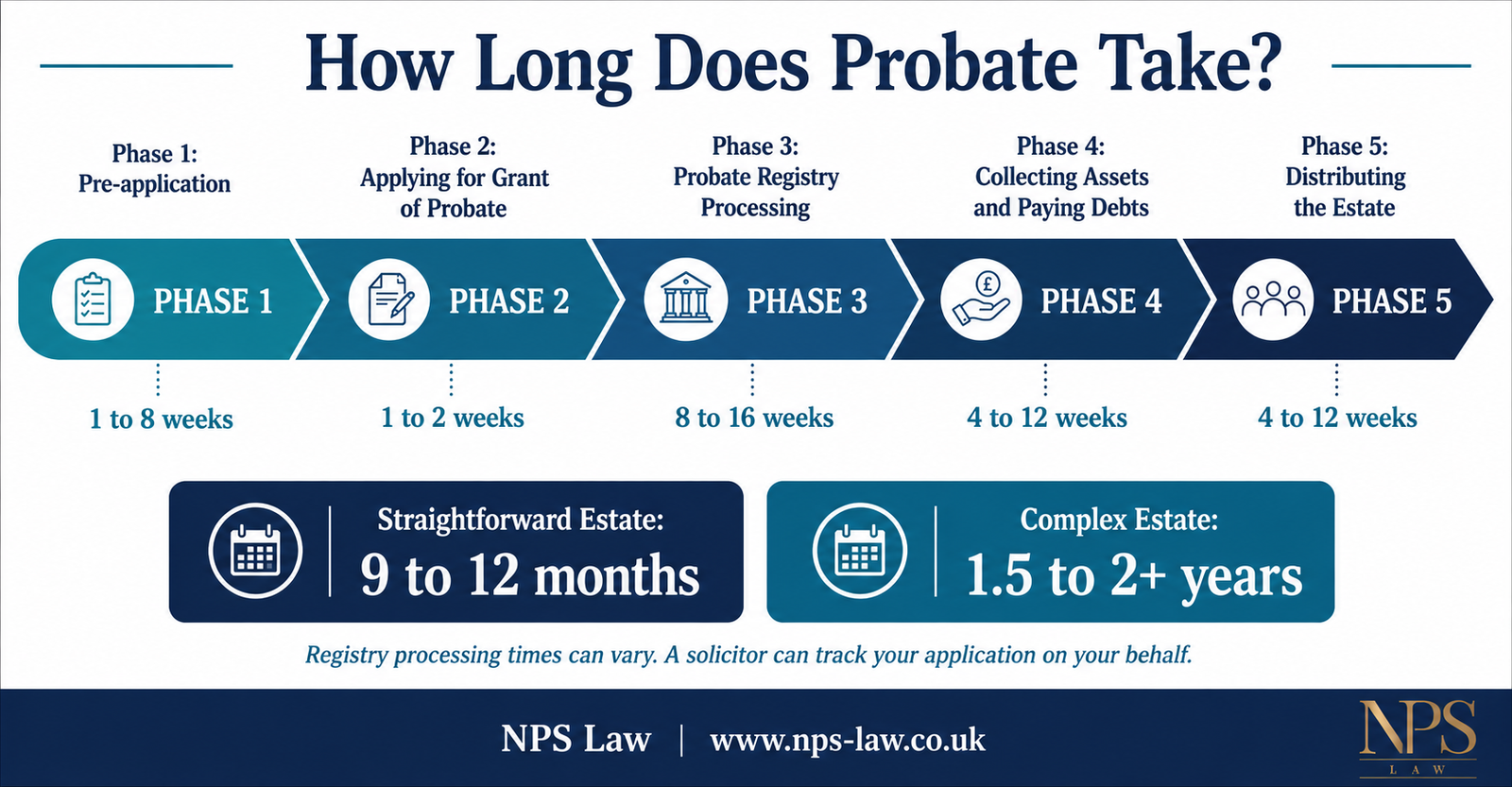

The timeline varies considerably depending on the complexity of the estate, whether inheritance tax is due, and current processing times at the Probate Registry. The table below gives realistic estimates for each stage.

| Stage | Typical Timeframe | What Can Extend It |

|---|---|---|

| Register death and locate will | 1 to 2 weeks | Contested death certificates; will stored securely offsite |

| Value the estate | 2 to 8 weeks | Multiple properties; overseas assets; unlisted shares |

| Report IHT and pay tax | 2 to 6 weeks | Complex IHT calculations; use of instalment option |

| Submit probate application | 1 to 2 weeks | Incomplete documentation |

| Probate Registry processing | 8 to 16 weeks | High application volumes; queries raised by the registry |

| Collect assets and pay debts | 4 to 12 weeks | Disputed debts; property sale delays |

| Gazette notice waiting period | 2 months and 1 day | Fixed statutory period |

| Distribute and close estate | 4 to 12 weeks | Beneficiary disputes; missing beneficiaries |

| Total (straightforward estate) | 9 to 12 months | |

| Total (complex estate) | 1.5 to 2+ years | Contentious probate; overseas assets; IHT disputes |

Probate Registry processing times have fluctuated significantly in recent years. At the time of writing, straightforward applications are being processed within eight to twelve weeks, though this can be longer during busy periods. A solicitor can track your application and chase the registry if delays occur.

Probate costs fall into three categories: the court fee, any professional fees, and the executor’s reasonable out-of-pocket expenses. All of these are paid from the estate itself; the executor is not personally liable for them.

Professional fees vary by firm and by the nature of the estate. Most solicitors charge either a fixed fee for straightforward cases or a percentage of the estate value for complex ones. As a general guide:

| Approach | Typical Cost | Best Suited To |

|---|---|---|

| DIY (no solicitor) | Court fee only (£300) | Simple estate, no property, no IHT, single beneficiary |

| Fixed-fee solicitor | £1,500 to £5,000 | Modest estate with property; executor wants certainty on costs |

| Percentage-based solicitor | 1% to 3% of estate value | Large or complex estate; multiple assets or beneficiaries |

| Full estate administration | 2% to 5% of estate value | Executor wants to hand over all duties entirely |

Using a solicitor does not mean handing over control. Many families choose to handle straightforward parts themselves, such as notifying utility companies or arranging the funeral, and instruct a solicitor only for the legal and tax elements.

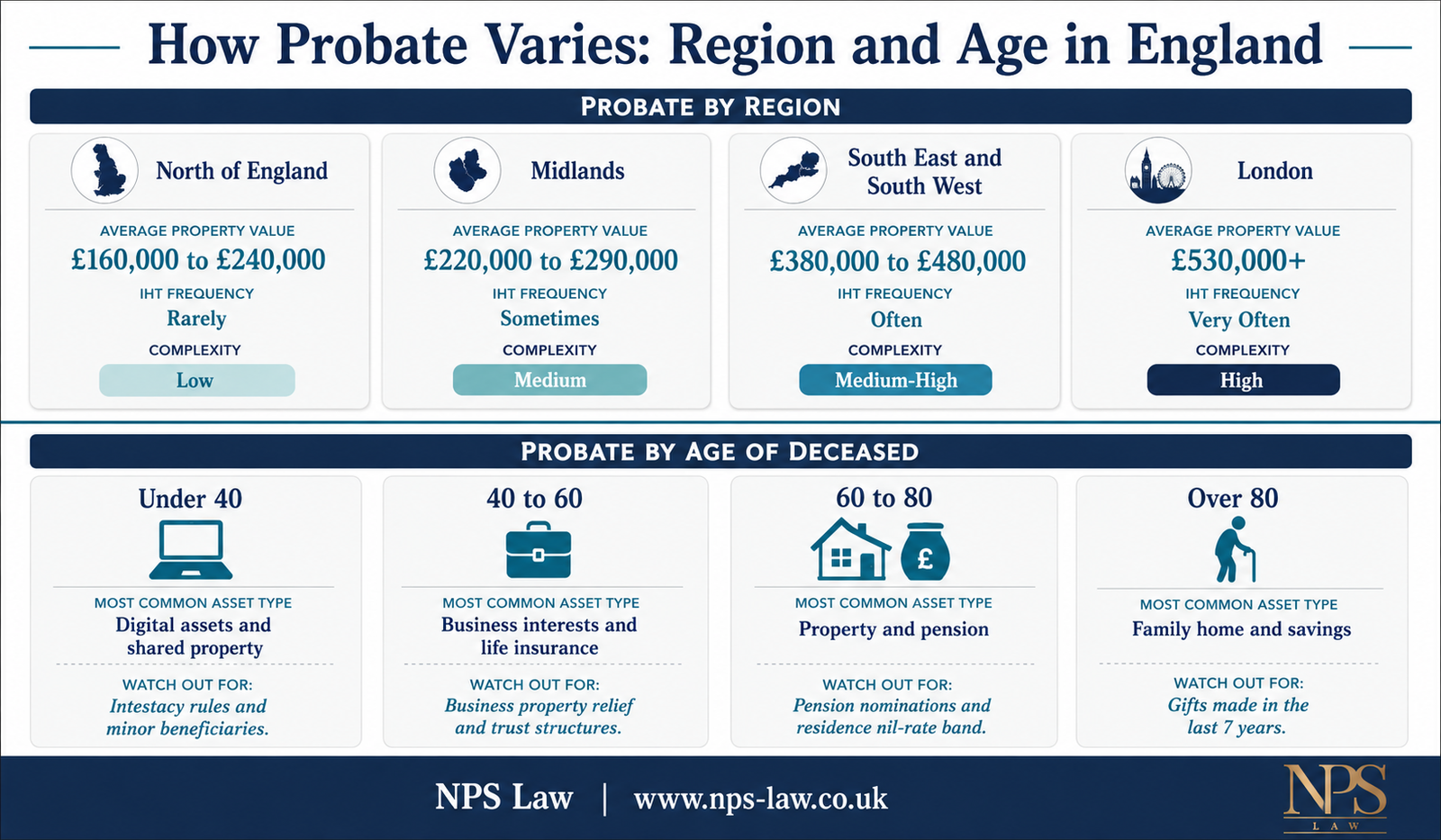

The legal framework for probate is the same across England and Wales, but practical differences in property values, local court workloads and the demographics of estates mean that the experience of going through probate can vary considerably.

| Region | Average Property Value (2025) | Typical Probate Considerations |

|---|---|---|

| London | £530,000+ | Estates frequently exceed IHT nil-rate band; residence nil-rate band (RNRB) often applies; property valuations require specialist agents; higher legal fees |

| South East and South West | £380,000 to £480,000 | Many estates cross the IHT threshold; agricultural property relief may apply in rural areas; probate property sales can be slower in rural markets |

| Midlands | £220,000 to £290,000 | Estates less frequently liable for IHT; business property relief relevant in manufacturing and logistics estates; generally shorter probate timelines |

| North (Yorkshire, North East, North West) | £160,000 to £240,000 | Majority of estates fall below IHT threshold; simpler applications more common; leasehold properties in urban areas can add complexity |

Property values are averages based on Land Registry data and vary significantly within each region. The IHT nil-rate band is £325,000 per person (or up to £650,000 for married couples and civil partners), with an additional residence nil-rate band of up to £175,000 per person when a family home passes to direct descendants.

| Age of Deceased | Common Asset Types | Typical Probate Complexities |

|---|---|---|

| Over 80 | Primary residence, savings, pension, personal possessions | Possible care home fee reclaims; mental capacity questions if will was made late in life; long history of gifts to family (7-year rule applies) |

| 60 to 80 | Property, ISAs, defined benefit pension, shares | Pension death benefits (usually outside estate but require nomination review); potential use of residence nil-rate band; property equity often substantial |

| 40 to 60 | Mortgage, life insurance, business interests, investments | Life insurance in trust passes outside estate; business property relief if self-employed or a shareholder; younger beneficiaries may require trusts if under 18 |

| Under 40 (unexpected death) | Rental or shared property, digital assets, student debt | Joint tenancy vs tenants in common critical; digital assets (crypto, online accounts) often overlooked; intestacy rules frequently apply; young children as beneficiaries require a trust |

| Beneficiary Age | Key Consideration | What the Executor Must Do |

|---|---|---|

| Under 18 | Cannot receive assets directly | Assets must be held in a statutory trust until age 18 (or age stated in will). Executor becomes trustee. |

| 18 to 25 | May receive outright or on deferred trust | Check will for conditions (e.g. 'at age 21'). Executor remains trustee until condition is met. |

| Adult (25+) | Receives outright | Standard distribution. Obtain signed receipt for each asset transferred. |

| Elderly beneficiary with reduced capacity | May lack capacity to manage inherited assets | Consider Court of Protection involvement; a lasting power of attorney held by someone else may already be in place. |

When someone dies without a valid will, they are said to have died intestate. Their estate is distributed according to the rules of intestacy, which set out a fixed order of inheritance.

Unmarried partners, cohabitees and friends have no automatic right to inherit under the intestacy rules, regardless of how long they lived together. If you were financially dependent on the deceased, you may be able to make a claim under the Inheritance (Provision for Family and Dependants) Act 1975, but this requires a separate court application.

If the deceased was married or in a civil partnership, the surviving partner inherits the first £322,000 of the estate plus all personal possessions outright. Anything above that is split equally between the surviving partner and any children.

If there is no surviving spouse or civil partner, the estate passes in full to children equally. If any child has predeceased the testator but had children of their own, those grandchildren take their parent’s share.

Most estates go through probate without serious difficulty, but some situations are more complex than others.

If several versions of a will exist, only the most recent valid one is used. If you suspect a more recent will exists but cannot find it, do not proceed until a thorough search has been completed, including checking with any solicitor the deceased used in later life.

HMRC can challenge asset valuations, particularly for property and private company shares. Executors who undervalue assets risk interest charges and penalties. A specialist valuation at the outset is considerably less expensive than a dispute later.

Disagreements between beneficiaries over the interpretation of a will, the fairness of a distribution, or the validity of the will itself are known as contentious probate. These disputes can halt the estate administration entirely until resolved. Mediation is usually faster and less costly than litigation.

Cryptocurrency, online investment accounts, domain names and digital businesses form part of the estate but are frequently overlooked. Access can be impossible without passwords or recovery keys. Executors should ask whether the deceased kept a record of digital accounts and check email archives for account confirmation messages from financial platforms.

An executor named in a will is not legally obliged to act. They can renounce probate before taking any steps in the administration. If no substitute is named and no other executor is willing to act, a beneficiary can apply to the court to be appointed administrator instead.

Applications have at times faced significant backlogs at the Probate Registry. Submitting a complete, accurate application the first time avoids queries that reset the clock. A solicitor who works with the registry regularly will know what is required and how to present it clearly.

You are not legally required to use a solicitor for probate. Executors can apply and administer the estate themselves. Whether it makes sense to do so depends on the complexity of the estate and your own confidence in dealing with legal and tax paperwork.

Executor mistakes can result in personal liability. If you distribute assets before paying all debts and taxes, or make an error in an IHT return, you may be required to make up the shortfall from your own pocket. Professional advice at the outset protects both the estate and the executor.

NPS Law offers a full probate and estate administration service covering everything from the initial application through to final distribution. Whether you need full support or just want guidance on a specific stage, our team is here to help.

NPS Law’s probate solicitors are here to help. Whether you need full estate administration or simply want to check you are on the right track, contact us today for a free initial conversation.

Probate is granted when the deceased left a valid will naming executors. Letters of administration are granted when there is no will, no living executor named in the will, or the named executor has renounced. The powers granted are identical; only the terminology and the route to obtaining them differ.

Most banks will release modest funds to cover immediate expenses, particularly funeral costs, before probate is obtained. Beyond that, accessing or transferring funds requires the grant. The exact amount each bank will release varies; contact them directly with the death certificate to ask.

All reasonable costs of administering an estate, including court fees and solicitors’ fees, are paid from the estate. The executor is not personally responsible for these costs unless they have acted improperly.

Yes, but the grounds are limited: fraud, forgery, lack of mental capacity, undue influence, or failure to comply with the formal requirements for executing a will. A challenge after the grant has been issued requires the grant to be revoked, which is a court process. Time limits apply, so anyone considering a challenge should seek legal advice promptly.

Digital assets that have monetary value, such as cryptocurrency holdings, online investment accounts or a monetised website, form part of the deceased’s estate and pass through probate in the same way as any other asset. Assets that are purely personal, such as social media accounts or email, do not form part of the estate but the executor may need to contact the platforms to close or memoralise them.

If the sole executor dies during administration, the estate does not automatically transfer to anyone. A new application must be made to the court for a grant of letters of administration with the will annexed. If there is a substitute executor named in the will, that person can apply instead.

Probate is the legal process of proving a will is valid, appointing an executor or administrator, valuing the estate, paying any inheritance tax and debts, and distributing what remains to the beneficiaries. In England and Wales it is overseen by the Probate Registry, and most straightforward estates are completed within nine to twelve months.

The process involves more complexity than many families expect, particularly where property is involved, where the estate crosses the inheritance tax threshold, or where the deceased left no will. Regional differences in property values mean that families in London and the South East face IHT considerations far more frequently than those in the North or Midlands, while the ages of both the deceased and the beneficiaries can affect everything from which assets are in the estate to whether a trust must be established before any funds can be released.

Whether you intend to manage the process yourself or would prefer professional support, understanding the steps involved and the decisions that need to be made at each stage is the best foundation for getting it right.

NPS Law offers expert probate and estate administration services across England and Wales. Visit our Wills and Probate service page or contact our team today for a free initial conversation.

The following sources were used in the preparation of this article. All links were verified at the time of publication. Government guidance and bank policies are subject to change; readers are advised to confirm current requirements directly with the relevant institution or authority.

Source | URL |

|---|---|

GOV.UK — Applying for probate | https://www.gov.uk/applying-for-probate |

GOV.UK — Inheritance Tax overview | https://www.gov.uk/inheritance-tax |

GOV.UK — Who inherits if someone dies without a will (intestacy) | https://www.gov.uk/inherits-someone-dies-without-will |

GOV.UK — Tell Us Once service | https://www.gov.uk/after-a-death/organisations-you-need-to-contact-and-tell-us-once |

GOV.UK — Paying Inheritance Tax | https://www.gov.uk/paying-inheritance-tax |

GOV.UK — Register a death | https://www.gov.uk/register-a-death |

GOV.UK — Form PA1P: Apply for probate (with will) | https://www.gov.uk/government/publications/form-pa1p-apply-for-probate-the-deceased-had-a-will |

GOV.UK — Form PA1A: Apply for probate (without will) | https://www.gov.uk/government/publications/form-pa1a-apply-for-probate-deceased-did-not-leave-a-will |

GOV.UK — HMRC Inheritance Tax nil-rate band guidance | https://www.gov.uk/government/collections/inheritance-tax |

GOV.UK — Direct Payment Scheme (paying IHT from deceased’s account) | https://www.gov.uk/paying-inheritance-tax/deceaseds-bank-account |

GOV.UK — How to obtain probate (guide for unrepresented applicants) | https://www.gov.uk/government/publications/how-to-obtain-probate-a-guide-for-people-acting-without-a-solicitor |

HM Land Registry — UK House Price Index | https://www.gov.uk/government/collections/uk-house-price-index-reports |

Source | URL |

|---|---|

The Gazette — Deceased estates notice guidance | https://www.thegazette.co.uk/wills-and-probate |

Legislation.gov.uk — Administration of Estates Act 1925 | https://www.legislation.gov.uk/ukpga/Geo5/15-16/23/contents |

Legislation.gov.uk — Inheritance (Provision for Family and Dependants) Act 1975 | https://www.legislation.gov.uk/ukpga/1975/63/contents |

Legislation.gov.uk — Inheritance and Trustees’ Powers Act 2014 | https://www.legislation.gov.uk/ukpga/2014/16/contents |

Note on bank thresholds: The probate thresholds listed for individual banks are based on publicly available information and industry practice at the time of writing. Each institution applies its own internal policy, which may change without notice. Always confirm the current threshold directly with the bank before beginning your application.

©️ Copyright 2026 NPS Law is a trading name for NPS Law LLP. Solicitors of England and Wales. Authorised and Regulated by the Solicitors Regulation Authority. SRA Number 570169. A list of all Partners is available on the SRA directory for this firm. website designed by origin-media