✓ Transfer of equity changes who owns a property — without selling it

✓ It is commonly triggered by divorce, marriage, gifting to family, or buying out a co-owner

✓ Costs typically range from £500 to £2,000+ depending on whether a mortgage is involved

✓ Stamp Duty Land Tax may apply — but is fully exempt in divorce settlements

✓ A solicitor is not legally required but is essential if there is a mortgage on the property

✓ NPS Law offers fixed-fee transfer of equity services across England and Wales

A transfer of equity is one of those legal processes that tends to appear at a significant moment in life — a divorce, a marriage, a death in the family, or a decision to restructure property ownership. Whatever the reason, it is important to understand the process, the costs involved, and when you need a solicitor to help you through it.

This guide covers everything you need to know about transfer of equity in the UK in 2026, from the step-by-step process to the tax implications, written in plain English by NPS Law’s specialist property solicitors.

A transfer of equity is the legal process of changing who owns a property by adding or removing a person from the title deeds — without selling the property outright. At least one of the original owners must remain on the title after the transfer.

This is different from a property sale, where the property is transferred entirely to a new owner. In a transfer of equity, the property stays in at least partial ownership of the existing owner, but the legal title changes.

Key Fact: Transfer of equity is not the same as equity release. Equity release is a financial product for homeowners aged 55+. Transfer of equity is a legal change of property ownership.

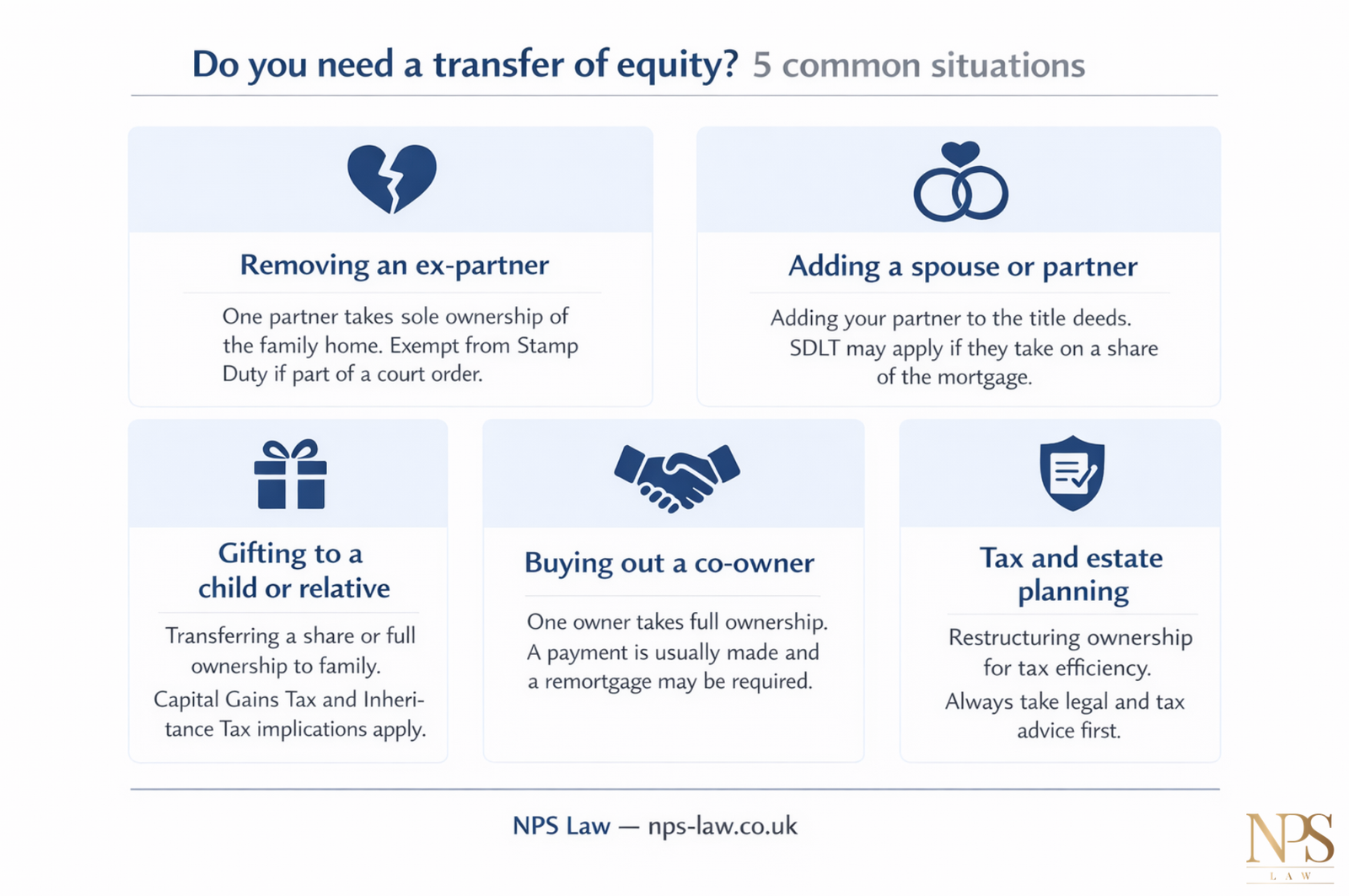

Transfer of equity arises in a range of circumstances, most of which involve a significant life event. Here are the most common situations:

When a relationship ends, one of the most common outcomes is that one partner takes sole ownership of the family home. This requires removing the other party’s name from the title deeds — a transfer of equity. If there is a mortgage on the property, the remaining owner will need to demonstrate they can afford the repayments alone, and the lender’s consent is required.

Many couples choose to add their partner’s name to the title deeds of a property they already own. This is a transfer of equity, and it can have implications for Stamp Duty Land Tax, particularly if the incoming partner takes on a share of the mortgage.

Parents sometimes transfer a share — or the entirety — of a property to their children, either as a gift or as part of inheritance planning. This is a transfer of equity and can have significant Capital Gains Tax and Inheritance Tax implications that should be discussed with a solicitor before proceeding.

Where two people jointly own a property and one wishes to take sole ownership, the departing owner’s share must be formally transferred. This may involve a payment to the departing owner and, if there is a mortgage, the ongoing owner will need to remortgage in their own name.

Some property owners transfer equity to restructure ownership for tax efficiency — for example, placing a property into joint ownership with a spouse to use both partners’ personal tax allowances. This should always be carried out with the guidance of both a solicitor and a tax adviser.

The total cost of a transfer of equity depends on several factors, including whether there is a mortgage on the property, the property’s value, and the complexity of the transaction. Here is a full breakdown:

| Cost | Typical Range (2026) |

|---|---|

| Solicitor's legal fees | £300 – £600 + VAT |

| Land Registry fee | £50 – £920 (based on property value) |

| Stamp Duty Land Tax | 0% – 5% (see below) |

| Mortgage lender consent fee | £0 – £300 (lender dependent) |

| Remortgage costs (if applicable) | £500 – £2,000 |

| ID verification checks | £10 – £50 |

| Bank transfer fee | £20 – £50 |

| Freeholder consent (leasehold only) | £50 – £200 |

For a straightforward transfer of equity without a mortgage, total costs are typically between £500 and £800 including disbursements. Where a mortgage is involved, or where a simultaneous remortgage is required, costs can rise to £1,500 to £3,000 or more.

NPS Law: We offer fixed-fee transfer of equity services with a full written breakdown of all costs before you instruct us. No hidden charges.

Whether Stamp Duty Land Tax (SDLT) is payable on a transfer of equity depends on the nature of the transfer — specifically, whether there is a “chargeable consideration” involved.

SDLT may be payable if the incoming owner takes on a share of the mortgage, pays money for the equity, or both. The tax is calculated on the value of the consideration — not the full property value.

Example: A property is worth £400,000 with an outstanding mortgage of £200,000. One partner transfers their 50% share to the other. The remaining owner takes on the full mortgage (£200,000). SDLT is calculated on £200,000 — the value of the mortgage assumed.

| Chargeable consideration | SDLT rate | Notes |

|---|---|---|

| Up to £250,000 | 0% | No SDLT payable |

| £250,001 – £925,000 | 5% | On the portion above £250,000 |

| £925,001 – £1.5m | 10% | On the portion above £925,000 |

| Above £1.5m | 12% | On the portion above £1.5m |

Transfer to a spouse or civil partner: Transfers between spouses who are living together are generally exempt.

Important: SDLT rules are complex and depend heavily on individual circumstances. Always seek legal advice before proceeding with a transfer of equity to understand your tax position.

If there is a mortgage on the property, the transfer of equity process becomes more complex. Here is what you need to know:

Your mortgage lender must agree to the transfer before it can proceed. The lender will typically carry out an affordability assessment on the remaining owner to confirm they can service the mortgage alone. This can add several weeks to the process.

In many cases — particularly where the departing owner is being released from the mortgage — it is necessary to remortgage at the same time as the transfer. Your solicitor can manage both processes simultaneously, and NPS Law can handle the full transaction under one roof.

Your solicitor must be on your lender’s approved panel to act in a remortgage transaction. NPS Law is on the panel for all major UK lenders.

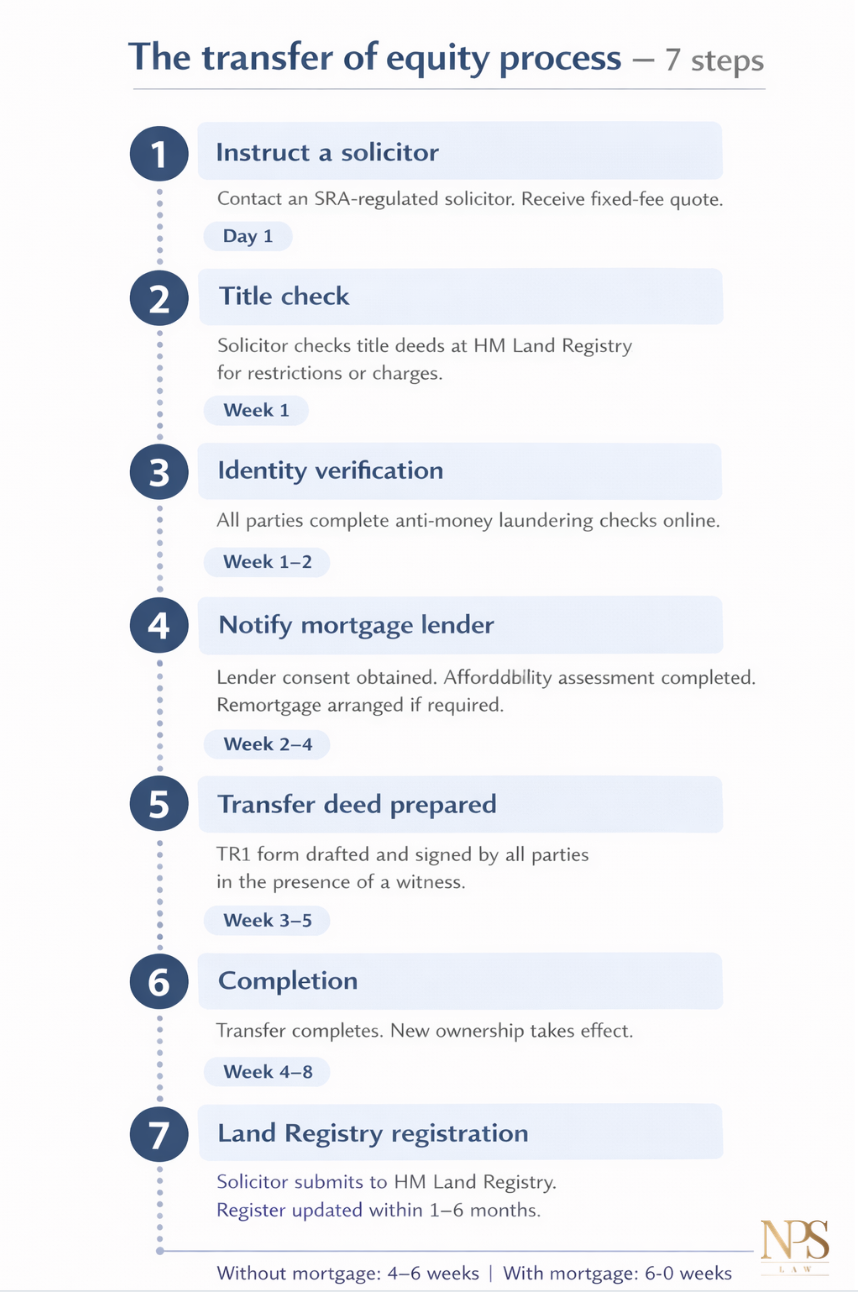

A straightforward transfer of equity typically takes between 4 and 8 weeks. Here is what happens at each stage:

Timeline: A simple transfer of equity without a mortgage typically completes in 4 to 6 weeks. With a mortgage or simultaneous remortgage, allow 6 to 10 weeks.

You are not legally required to use a solicitor for a transfer of equity. However, instructing a qualified solicitor is strongly recommended in almost every case — and is a practical necessity if there is a mortgage on the property.

Here is why a solicitor is essential:

Speak to NPS Law’s transfer of equity team today for a free, no-obligation quote. nps-law.co.uk/contact

Transfer of equity in divorce is one of the most sensitive and complex situations. The key points to understand are: transfers under a court order are exempt from SDLT; each party should have independent legal representation; and the remaining owner will need to demonstrate mortgage affordability to the lender. NPS Law can advise on all aspects of the transfer, and our wills and probate team can also assist with updating wills and other documents as part of the settlement.

Adding a partner to your title deeds is a positive step, but it carries legal and financial consequences for both parties. The incoming partner takes on legal responsibility for the property, and SDLT may be payable if they are assuming a share of the mortgage. A Declaration of Trust setting out each party’s beneficial interest is also worth considering at this stage.

Gifting property or a share of property to a family member can be an effective estate planning tool — but the tax implications are significant. Capital Gains Tax may be payable on any increase in value since you bought the property. Inheritance Tax rules also apply if the gift is made within seven years of your death. Always take legal and tax advice before proceeding.

If a co-owner has died and the property was held as joint tenants, ownership passes automatically to the surviving owner by survivorship — no transfer of equity is required, but the title still needs to be updated at the Land Registry. If the property was held as tenants in common, the deceased’s share forms part of their estate and must be dealt with through probate. NPS Law handles both property transfers and probate, meaning we can manage the entire process under one roof.

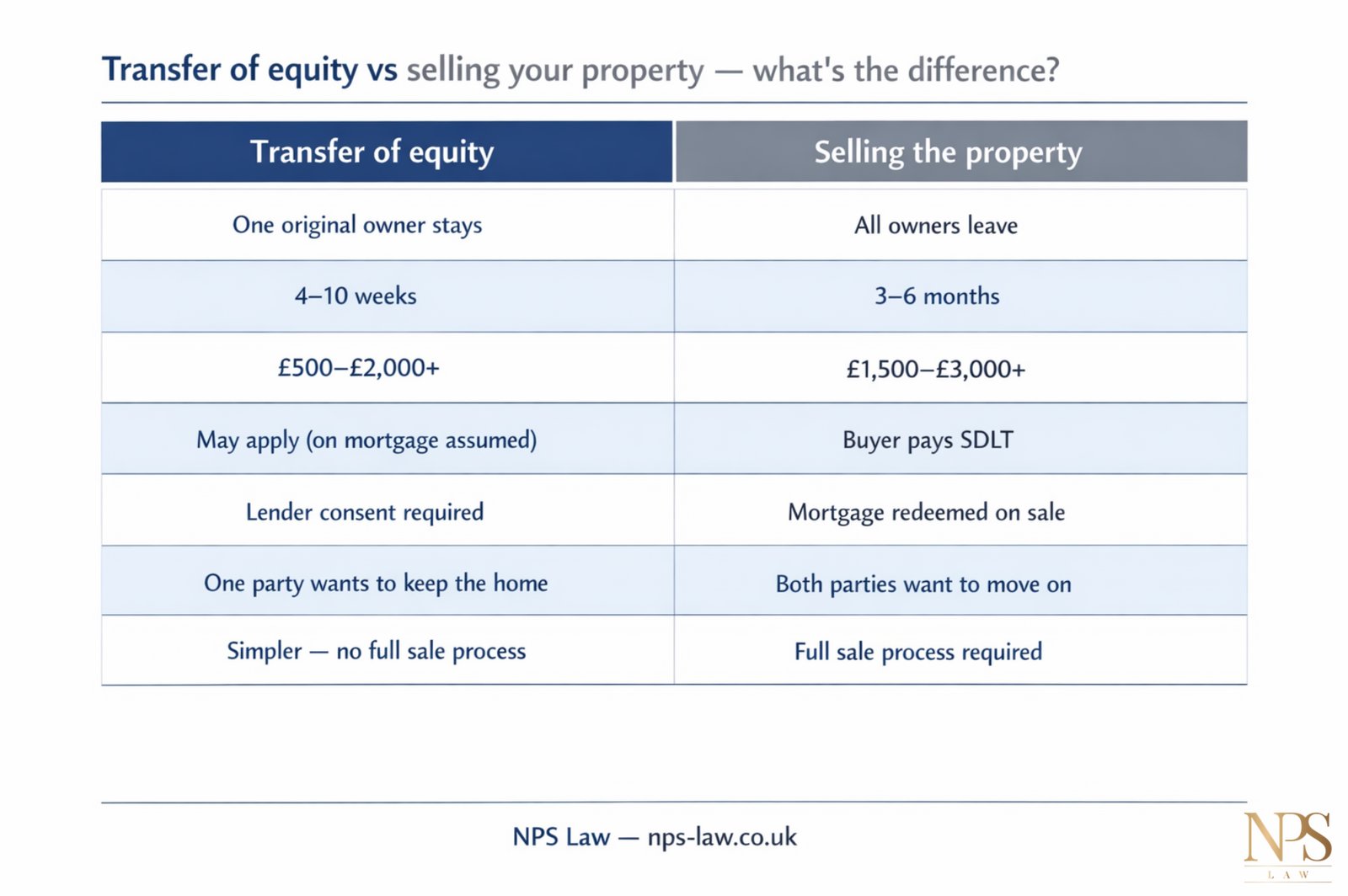

When a relationship breaks down or co-owners wish to go their separate ways, there are two main options: a transfer of equity (where one party keeps the property) or a sale (where the property is sold and the proceeds divided). Here is how they compare:

| Transfer of Equity | |

|---|---|

| Ownership | One original owner stays on the title |

| Process time | 4 – 10 weeks |

| Legal costs | £500 – £2,000+ |

| SDLT | May apply (see above) |

| Mortgage | Lender consent required — may need to remortgage |

| Best for | One party wants to keep the home |

| Emotional impact | Can be simpler — avoids a full sale |

The right choice depends on your individual circumstances, including whether you can afford the mortgage alone, the current property value, and the tax implications of each option. NPS Law can advise you on both routes.

NPS Law is a specialist property law firm with offices across the Midlands and full remote capability for clients anywhere in England and Wales. Our transfer of equity team has extensive experience handling transactions of all complexity levels — from straightforward additions of a partner to complex divorce-related transfers with simultaneous remortgages.

Ready to get started? Get your free transfer of equity quote from NPS Law today. nps-law.co.uk

The information in this guide applies to transfer of equity transactions in England and Wales only. The legal system in Scotland operates differently — property law in Scotland is governed by Scots law, and the process for changing ownership is handled through a system of missives rather than title deeds. If your property is in Scotland, you will need a Scottish solicitor.

In England and Wales, NPS Law can handle transfer of equity transactions for properties anywhere in the country, whether you are based near our Midlands offices or anywhere else in England and Wales.

Transfer of equity is the legal process of adding or removing a person from the ownership of a property without selling it. At least one of the original owners must remain on the title after the transfer.

Total costs typically range from £500 to £2,000 or more, depending on whether a mortgage is involved, the value of the property, and the complexity of the transaction. Costs include solicitor’s fees, Land Registry fees, and potentially Stamp Duty Land Tax. NPS Law provides fixed-fee quotes with no hidden extras.

It depends. SDLT may be payable if the incoming owner takes on a share of the mortgage or pays money for the equity. However, transfers made as part of a divorce settlement are fully exempt. Transfers between spouses who are living together are also generally exempt.

A straightforward transfer of equity without a mortgage typically takes 4 to 6 weeks. Where a mortgage is involved or a simultaneous remortgage is required, allow 6 to 10 weeks. Complex transactions — such as those involving disputed ownership or leasehold complications — may take longer.

You are not legally required to use a solicitor, but it is strongly recommended. If there is a mortgage on the property, the lender will require a solicitor on their approved panel. A solicitor also ensures the title is correct, the SDLT position is properly assessed, and all parties are protected.

If there is a mortgage on the property, your lender must consent to the transfer. They will typically carry out an affordability assessment on the remaining owner. In many cases, particularly where the departing owner needs to be released from the mortgage, a simultaneous remortgage in the remaining owner’s name is required.

No. In a transfer of equity, at least one original owner remains on the title. In a property sale, the property is transferred entirely to a new owner. Transfer of equity is appropriate where one party wants to keep the home; a sale is appropriate where both parties want to move on completely.

This article is for general informational purposes only and does not constitute legal advice. Tax rules and regulations are subject to change. Always seek independent legal and tax advice for your specific circumstances. NPS Law is regulated by the Solicitors Regulation Authority (SRA). SDLT rates sourced from gov.uk/stamp-duty-land-tax. Land Registry fees sourced from gov.uk/registering-land-or-property-with-land-registry.

©️ Copyright 2026 NPS Law is a trading name for NPS Law LLP. Solicitors of England and Wales. Authorised and Regulated by the Solicitors Regulation Authority. SRA Number 570169. A list of all Partners is available on the SRA directory for this firm. website designed by origin-media