✓ An Energy Performance Certificate (EPC) is a legal requirement before marketing a property for sale or rent in England and Wales

✓ EPCs are valid for 10 years and must be obtained from an accredited domestic energy assessor

✓ Your conveyancing solicitor will check your EPC as part of the property transaction

✓ In 2026, the UK government’s Warm Homes Plan is driving stricter EPC requirements for landlords and sellers

✓ Properties with EPC ratings of C or above may qualify for preferential green mortgage rates

✓ Failure to provide a valid EPC when selling can result in a fine of up to £5,000

✓ NPS Law handles all EPC-related aspects of your conveyancing — including flagging issues before they delay your sale

If you are buying or selling a property in England or Wales, an Energy Performance Certificate — or EPC — is one of the first legal requirements you will encounter. Yet many buyers and sellers are unclear about exactly how an EPC fits into the conveyancing process, what the current rules require, and what happens if something goes wrong.

This guide, written by NPS Law’s specialist property team, explains everything you need to know about EPCs and conveyancing in 2026 — from the legal requirements and costs to the impact of the government’s new energy efficiency targets on your transaction.

An Energy Performance Certificate is an official document that records the energy efficiency of a property. It is produced by an accredited domestic energy assessor who visits the property and evaluates factors including insulation, heating systems, windows, and lighting.

The assessor assigns the property an energy efficiency rating on a scale from A to G, where A is the most energy efficient and G is the least. The certificate also includes a list of recommended improvements, an estimate of how much those improvements would cost, and the potential energy savings they would generate.

EPCs were introduced in England and Wales in 2007 as part of the government’s efforts to improve energy efficiency across the housing stock. Since then, they have become a fundamental part of every property transaction.

| EPC Rating | Energy Efficiency |

|---|---|

| A | Very energy efficient — lowest running costs |

| B | Highly energy efficient |

| C | Good energy efficiency — increasingly required by lender |

| D | Average — most UK properties fall here |

| E | Below average — minimum for rental properties |

| F | Poor — cannot legally be rented out |

| G | Very poor — cannot legally be rented out |

Key Fact: An EPC is valid for 10 years from the date of issue, unless a new certificate is produced for the same property. You can check whether a property has a valid EPC for free at gov.uk/find-energy-certificate.

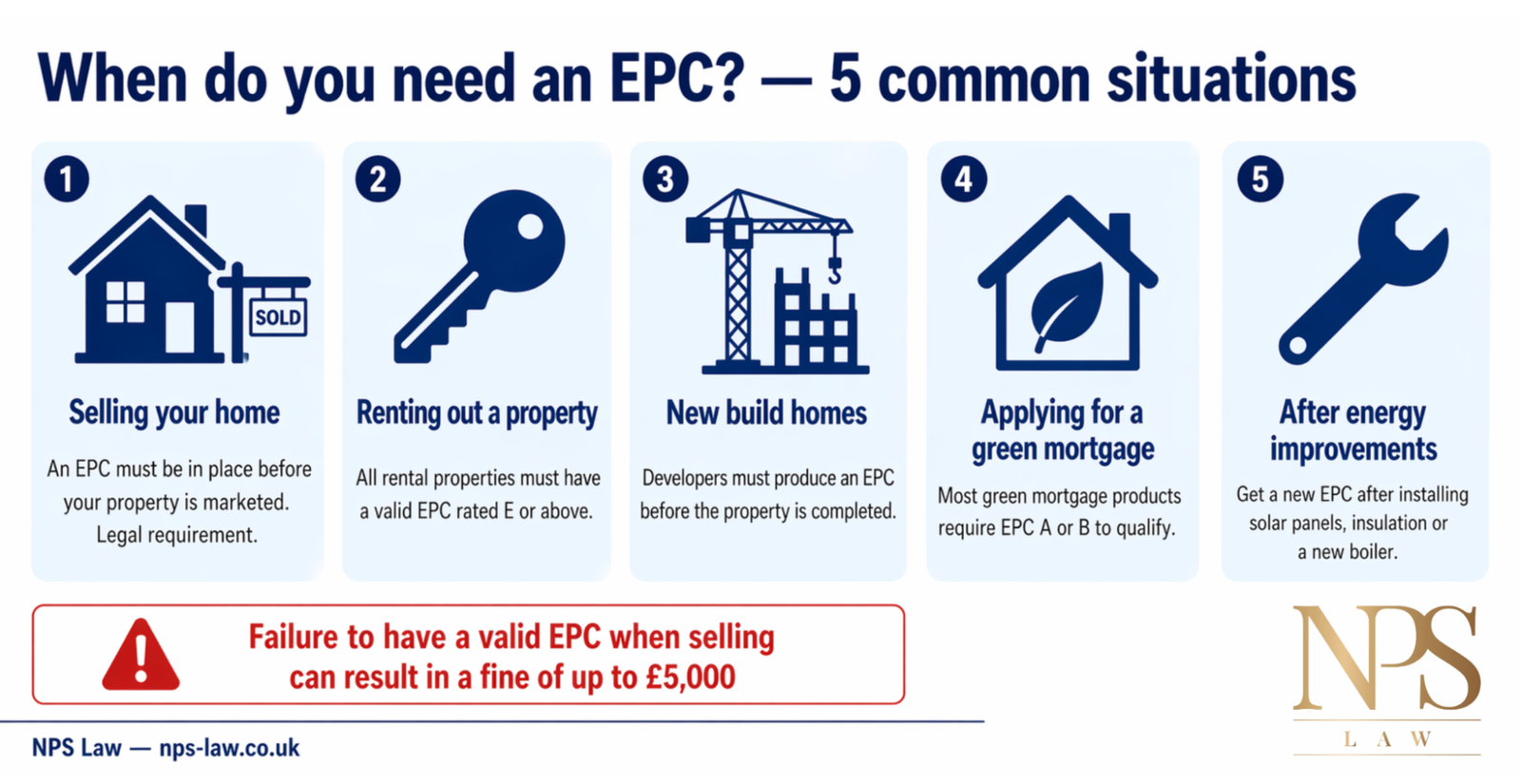

An EPC is legally required in a number of circumstances. Here are the situations where you must have a valid certificate in place:

If you are selling a residential property in England or Wales, you must have a valid EPC before the property is marketed — whether online, in an estate agent’s window, or in any other form of advertising. The EPC must be made available to prospective buyers free of charge. This is a legal requirement, not a recommendation.

Landlords must have a valid EPC for every property they let. The certificate must show a minimum rating of E or above. Properties rated F or G cannot legally be rented out, and landlords who fail to comply face fines of up to £30,000.

Developers must produce an EPC for every new build property before it is completed. New builds typically achieve higher EPC ratings due to modern insulation and heating standards.

While an EPC is not always legally required for a remortgage, many lenders now require a current EPC to process a green mortgage application. If your existing EPC has expired, you may need to commission a new one.

If you have carried out significant energy efficiency improvements — such as installing loft insulation, solar panels, or a new boiler — it is worth commissioning a new EPC to reflect the improvements. A better rating can support a higher property valuation and unlock green mortgage rates.

The EPC sits at the heart of the conveyancing process. Here is exactly how your solicitor interacts with your EPC during a property transaction:

As the seller, you must ensure a valid EPC is in place before your property is listed. Your conveyancing solicitor will request evidence of the EPC as part of the pre-contract pack. If your EPC has expired or does not exist, your solicitor will advise you to commission a new one before the transaction can proceed.

Your solicitor will also check the EPC for any issues that could affect the buyer’s mortgage offer or cause delays — for example, if the property is rated F or G and the buyer’s lender requires a minimum rating of E.

As the buyer, your conveyancing solicitor will review the seller’s EPC as part of their due diligence. The EPC rating can affect your mortgage offer — particularly if you are applying for a green mortgage — and your solicitor will flag any concerns before exchange of contracts.

If the EPC reveals that the property requires significant energy efficiency improvements, your solicitor can advise you on whether this should be reflected in the purchase price or whether you should negotiate with the seller.

For leasehold properties — such as flats — the EPC situation can be more complex. The certificate may cover only the individual flat, or it may cover the whole building. Your conveyancing solicitor will clarify which applies and ensure the correct certificate is in place.

Important: If your EPC has expired at the point of marketing your property, you are in breach of the Energy Performance of Buildings Regulations 2012. You must commission a new EPC before proceeding. Failure to do so can result in a fine of up to £5,000.

The energy efficiency landscape is changing rapidly in 2026. The government’s Warm Homes Plan, published in January 2026, sets out an ambitious programme to improve the energy efficiency of the UK’s housing stock — and the rules affecting sellers and landlords are evolving as a result.

The most significant development for sellers in 2026 is the increasing scrutiny applied to properties with low EPC ratings. While there is currently no legal requirement for sellers to achieve a specific EPC rating, buyers and mortgage lenders are placing greater weight on energy efficiency than ever before.

2026 Update: The UK government’s Warm Homes Plan sets a target for all homes to reach EPC Band C by 2030. While this is primarily a landlord obligation, the direction of travel is clear — energy efficiency is becoming a central factor in property transactions for all buyers and sellers.

Your EPC rating can have a material effect on how quickly your property sells and the price you achieve. Here is a breakdown of the key impacts by rating:

| EPC Rating | Impact on Sale | Lender Position |

|---|---|---|

| A – B | Fastest time to sell. Green mortgage eligible. Premium pricing possible. | All lenders — preferential green rates available |

| C | Strong buyer demand. Mortgage-friendly. Becoming the market standard. | All lenders — standard rates |

| D | Average. No immediate barriers but buyers may negotiate on price. | Most lenders — standard rates |

| E | Some buyer hesitation. Minimum standard for rental. May affect mortgage options. | Most lenders — check individual requirements |

| F – G | Significant barriers. Cannot be rented. Many lenders will not lend. | Limited lender options. Survey may flag issues. |

If your property’s EPC rating is lower than you would like, there are practical steps you can take before going to market. Your existing EPC will include a list of recommended improvements with estimated costs and savings. The most cost-effective improvements typically include:

Even modest improvements can push a property up one or two bands — which can make a significant difference to buyer demand and mortgage availability.

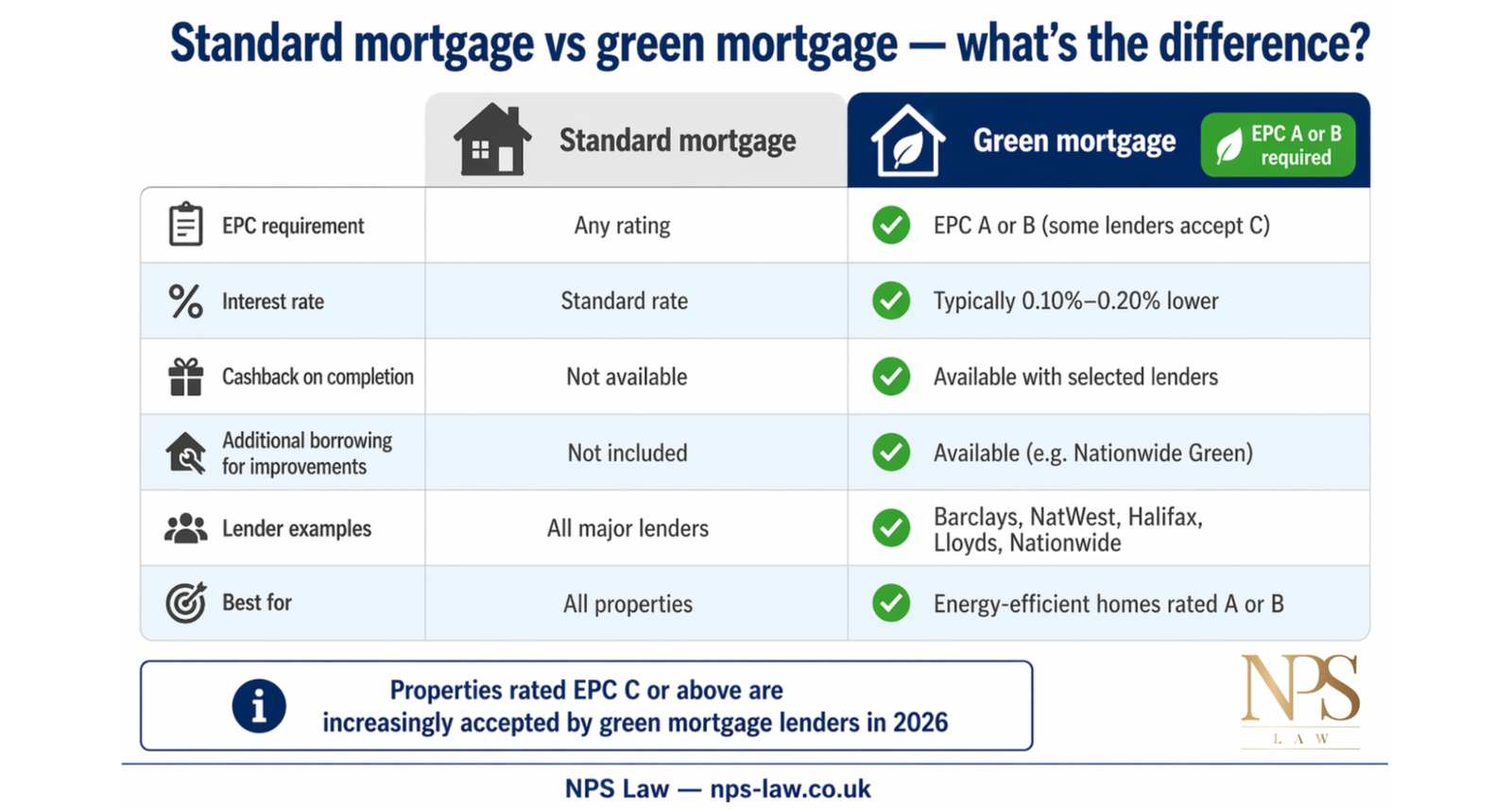

One of the most significant recent developments in the property market is the growth of green mortgages — mortgage products offered at preferential rates to buyers of energy-efficient properties. Understanding how EPCs interact with green mortgages is increasingly important for both buyers and sellers.

A green mortgage is a home loan offered at a lower interest rate or with other incentives — such as cashback — for properties that meet a minimum energy efficiency standard. Most green mortgage products require the property to have an EPC rating of A or B, though some lenders also offer incentives for properties rated C.

NPS Law: We are on the panel for all major mortgage lenders, including those offering green mortgage products. Our conveyancing team can advise you on how your EPC rating may affect your mortgage options as part of your transaction.

If you are a landlord, EPC compliance is not optional — it is a legal requirement with significant financial penalties for non-compliance. Here is what you need to know in 2026:

Under the Minimum Energy Efficiency Standards (MEES), all privately rented properties in England and Wales must have a valid EPC with a rating of at least E. This applies to all tenancies — new and existing — since April 2020.

Important: Landlords who let a property with an EPC rating of F or G without a valid exemption face fines of up to £30,000 per property. Enforcement notices are also published on the public PRS Exemptions Register.

The government’s Warm Homes Plan sets a target for all privately rented properties to achieve EPC Band C by 1 October 2030. This is a significant increase from the current Band E minimum and will require substantial investment from many landlords.

A £10,000 cost cap applies — if you spend this amount on energy efficiency improvements and your property still has not reached Band C, you can register an exemption for 10 years.

| Requirement | Details |

|---|---|

| Current minimum (all tenancies) | EPC Band E |

| 2030 target | EPC Band C |

| Maximum spend before exemption | £10,000 per property |

| Fine for non-compliance | Up to £30,000 per property |

| Exemption duration | 10 years (cost cap) or 5 years (other) |

| Scotland | Separate regime — check scottishepcregister.org.uk |

If you are selling a rental property, your EPC rating will be scrutinised by the buyer’s solicitor and their mortgage lender. A property that does not meet the current minimum standard may deter buyers or affect the purchase price. NPS Law’s conveyancing team can advise you on the most efficient way to manage the EPC position as part of the sale.

An EPC can only be produced by an accredited domestic energy assessor. The process is straightforward:

| Cost Factor | Typical Range |

|---|---|

| Standard EPC assessment | £60 – £120 |

| Large property (5+ bedrooms) | £100 – £150 |

| New EPC after improvements | £60 – £120 |

| Time from booking to certificate | 3 – 10 days |

Need guidance on EPC requirements as part of your sale or purchase? Speak to NPS Law today for a free, no-obligation quote. nps-law.co.uk/contact

An EPC that expires during the conveyancing process can cause delays — and in some cases, legal complications. Here is what to do if this happens:

If your EPC expires before exchange of contracts, you will need to commission a new one as quickly as possible. Your conveyancing solicitor will flag the issue and advise on the most efficient course of action. In most cases, a new EPC can be obtained within a week.

This is a less common situation, but it can occur in longer transactions. Your solicitor will advise on whether a new EPC is required and what steps to take to avoid delaying completion.

It is easy to overlook the expiry of an EPC — particularly if it was obtained 10 years ago when you first purchased the property. Your conveyancing solicitor will identify the issue early in the transaction and advise you promptly. Checking your EPC validity at gov.uk/find-energy-certificate before going to market is a simple step that avoids unnecessary delays.

Important: Always check your EPC validity before instructing an estate agent. An expired EPC must be renewed before your property can be legally marketed. Your conveyancing solicitor will confirm this as part of the pre-contract process.

Starting a sale or purchase? Contact NPS Law today and we will check your EPC position as part of our free initial review. nps-law.co.uk/contact

NPS Law is an SRA-regulated property law firm with specialist expertise in residential and commercial conveyancing across England and Wales. Our team has extensive experience handling all aspects of EPC compliance as part of property transactions — from identifying expired certificates to advising on the impact of low ratings on mortgage options.

Get your free conveyancing quote from NPS Law today — including a full EPC compliance check. nps-law.co.uk

Yes. You must have a valid EPC in place before your property is marketed for sale in England and Wales. This is a legal requirement under the Energy Performance of Buildings Regulations 2012. Failure to comply can result in a fine of up to £5,000.

An EPC is valid for 10 years from the date it is issued, unless a new certificate is produced for the same property before the 10 years are up. You can check the validity of an EPC at gov.uk/find-energy-certificate.

There is currently no minimum EPC rating required to sell a residential property in England or Wales. However, properties rated F or G may face difficulties with some mortgage lenders, and buyer demand for lower-rated properties is declining. The government’s 2030 target for rental properties is Band C.

Yes. If a buyer’s mortgage lender will not lend on a property due to its EPC rating, the buyer may be unable to proceed. Even where financing is available, a low EPC rating can prompt buyers to renegotiate the purchase price or withdraw from the transaction.

An EPC assessment typically costs between £60 and £120 for a standard residential property, depending on the size of the property and the assessor. The certificate is then valid for 10 years.

The current minimum EPC rating for privately rented properties in England and Wales is Band E. Properties rated F or G cannot legally be rented out. The government has set a target of Band C for all private rental properties by October 2030.

A new EPC is not always legally required for a remortgage. However, if you are applying for a green mortgage — which offers preferential rates for energy-efficient properties — your lender may require a current EPC to confirm your property’s rating. If your EPC has expired, a new assessment will be needed.

This article is for general informational purposes only and does not constitute legal advice. EPC regulations and government targets are subject to change. Always seek independent legal advice for your specific circumstances. NPS Law is regulated by the Solicitors Regulation Authority (SRA). EPC information sourced from gov.uk/find-energy-certificate and the Ministry of Housing, Communities and Local Government.

©️ Copyright 2026 NPS Law is a trading name for NPS Law LLP. Solicitors of England and Wales. Authorised and Regulated by the Solicitors Regulation Authority. SRA Number 570169. A list of all Partners is available on the SRA directory for this firm. website designed by origin-media