Losing a loved one is difficult enough. Having to navigate the legal and administrative process of probate at the same time can feel overwhelming. But understanding what probate involves — and what to expect at each stage — makes the process far more manageable.

This complete guide explains every step of the UK probate process in 2026, from registering the death through to distributing the estate. Whether you have been named as an executor in a will, or you are the next of kin applying for letters of administration, this guide covers everything you need to know.

For tailored advice from a qualified solicitor, NPS Law’s specialist probate team is here to help.

| Key Point | Details |

|---|---|

| Legal Authority | Probate grants the legal right to access and manage the deceased's estate |

| Eligibility | Only named executors (with a will) or closest relatives (without a will) can apply. |

| Court Fee | £300 for estates over £5,000 (free for smaller estates) — updated January 2025. |

| Typical Timeline | 4–16 weeks for the Grant; 6–18 months for full estate administration. |

| Solicitor vs DIY | DIY costs £300 in court fees. A solicitor typically charges 1–4% of the estate value. |

Probate is the legal process that gives you the authority to deal with a deceased person’s estate — their property, money, and possessions. In England and Wales, this authority comes in the form of an official document:

Without one of these documents, banks, the Land Registry, and other institutions will not allow you to access or transfer the deceased’s assets.

Do You Always Need Probate?

Not always. Whether probate is required depends on the type of assets and their value. Use the table below as a guide:

| Probate Usually Required | Probate Usually NOT Required |

|---|---|

| Property owned solely by the deceased | Jointly owned assets (pass automatically to the survivor) |

| Bank accounts above the institution's threshold | Bank accounts below the institution's threshold (typically £50,000) |

| Investments, shares, or ISAs in sole name | Assets in a trust |

| Estates with complex assets or debts | Life insurance with a named beneficiary |

Bank Probate Thresholds (2026)

Each bank sets its own threshold for releasing funds without probate. As of 2026, most major UK banks have aligned at £50,000 per institution. This threshold applies per institution, not to the total estate — so if the deceased held accounts at two separate banks below the threshold, probate may not be required for either.

| Bank / Building Society | Probate Threshold (2026) |

|---|---|

| Barclays | £50,000 |

| HSBC | £50,000 |

| Lloyds / Halifax | £50,000 (combined for same group) |

| NatWest / RBS | £50,000 |

| Santander | £50,000 |

| Nationwide | £50,000 |

| Note: | Thresholds apply per institution, not total estate. Always confirm directly with each bank. |

The person who applies depends on whether the deceased left a valid will.

The executor named in the will applies for the Grant of Probate. If more than one executor is named, they can apply jointly or one can act on behalf of all. If the named executor is unwilling or unable to act, they can formally renounce the role.

When someone dies without a will, they are said to have died intestate. In this case, a close relative — usually the spouse, civil partner, or adult child — applies for Letters of Administration using form PA1A. The estate is then distributed according to the Rules of Intestacy rather than the deceased’s wishes.

In both cases, the applicant must be over 18 and have the legal capacity to manage the estate.

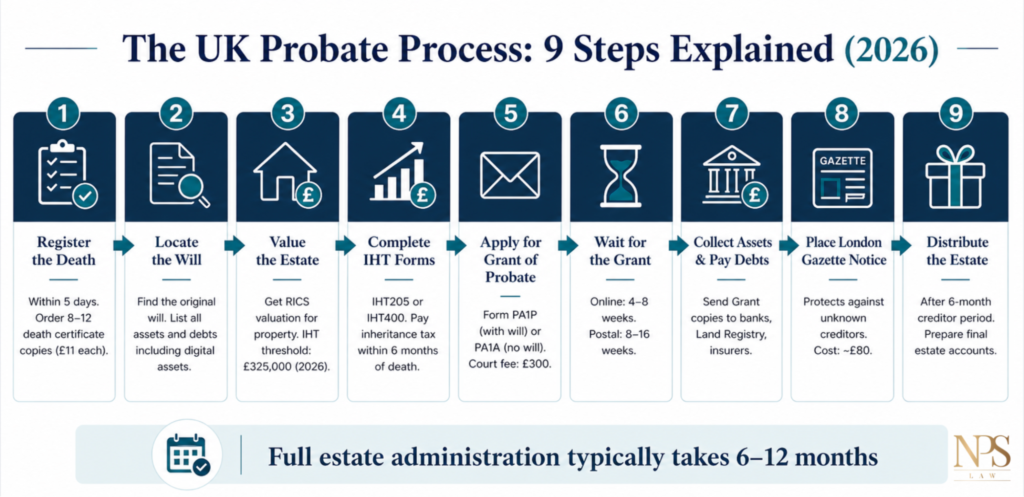

The UK probate process follows a broadly consistent sequence of stages. Here is what to expect at each step.

You must register the death within five days in England and Wales (eight days in Scotland). Registration is done at the local register office. You will receive a death certificate — order multiple certified copies at this stage, as banks, HMRC, and the Probate Registry will each require one. Copies cost £11 each; it is advisable to order at least eight to twelve.

Locate the original will, which may be held at home, with a solicitor, or registered with the National Will Register. Once you have the will, begin compiling a full inventory of the estate:

For digital assets such as cryptocurrency or online investment accounts, check for records of login details or a digital estate plan left by the deceased.

You must obtain accurate valuations of all assets as at the date of death. For residential property, HMRC may accept an estate agent’s valuation, but a professional RICS surveyor’s report is recommended — particularly for higher-value properties or where HMRC may scrutinise the figure. For investments and shares, use the closing price on the date of death.

The inheritance tax threshold (nil-rate band) for 2026 is £325,000. If the estate includes a residential property passing to direct descendants, an additional residence nil-rate band of up to £175,000 may apply.

Before applying for probate, you must report the estate’s value to HMRC and, if applicable, pay any inheritance tax due.

Inheritance tax (charged at 40% on the value above the threshold) must generally be paid within six months of death, before the Grant of Probate is issued. This can create a cash-flow challenge, as funds are frozen until probate is granted — your solicitor can advise on options including using the deceased’s bank accounts directly or estate loans.

Once the estate has been valued and inheritance tax dealt with, you can submit the probate application to HMCTS (His Majesty’s Courts and Tribunals Service). You will need:

You can apply online at gov.uk/applying-for-probate or by post. Online applications are processed significantly faster and are recommended for straightforward estates.

Once submitted, the Probate Registry will process your application. Current processing times in 2026 are:

You may be asked to attend an interview or provide additional documents. Applications are frequently returned for errors — incomplete forms, missing documents, or unsigned declarations are the most common causes of delay. Order additional sealed copies of the Grant at £1.50 each, as banks and the Land Registry will each require a copy.

With the Grant of Probate in hand, you now have legal authority to administer the estate. Send certified copies of the Grant to:

All debts — including mortgages, credit cards, and outstanding bills — must be settled before any distribution to beneficiaries. Keep detailed records of every transaction, as executors can be held personally liable for errors.

This step is not legally required but is strongly recommended. Placing a creditor notice in The London Gazette (and, ideally, a local newspaper) gives unknown creditors two months to come forward. Once that period has passed, you are protected against claims from creditors you were unaware of. The cost is approximately £80.

Once all debts and taxes have been paid and the creditor notice period has elapsed, you can distribute the remaining estate to the beneficiaries named in the will (or, if there is no will, according to the Rules of Intestacy). Prepare a final estate account showing all assets received, debts paid, and distributions made. Provide this account to the beneficiaries for their records.

The timeline varies significantly depending on the complexity of the estate, whether inheritance tax is payable, and how quickly institutions respond. As a general guide:

| Stage | Task | Typical Duration |

|---|---|---|

| 1 | Register death, gather documents | 1–2 weeks |

| 2 | Value the estate | 4–8 weeks |

| 3 | Complete IHT forms | 2–4 weeks |

| 4 | Submit probate application | 1 week |

| 5 | Wait for Grant of Probate | 4–16 weeks |

| 6 | Collect assets, pay debts | 1–3 months |

| 7 | Distribute estate to beneficiaries | 1–3 months |

| Total | Simple estate | 6–12 months |

Online applications process considerably faster than postal submissions. If the estate includes property to sell, allow an additional four to six months for conveyancing. Contested estates or those with foreign assets can take 18–24 months or more.

Executors carry personal liability for errors in estate administration. These are the most common mistakes and how to avoid them:

| Common Mistake | How to Avoid It |

|---|---|

| Undervaluing the estate | Use a professional RICS surveyor for property; get written valuations for all significant assets. |

| Submitting incomplete forms | Use the GOV.UK probate application checklist before submitting. 1 in 3 applications are returned for errors. |

| Distributing assets too early | Wait at least 6 months after the Grant before final distribution to allow creditor claims. |

| Failing to notify creditors | Place a notice in The London Gazette and a local newspaper to protect against unknown creditors. |

| Forgetting digital assets | Include cryptocurrency, PayPal balances, online investment accounts, and digital businesses in the estate valuation. |

Many people successfully handle straightforward probate themselves. However, professional support is strongly recommended in certain circumstances.

Cost comparison at a glance:

| DIY Probate | Probate Solicitor |

|---|---|

| Court fee only: £300 | 1–4% of estate value (typically £3,000–£12,000 on a £300,000 estate) |

| Suitable for simple estates with a clear will | Recommended for complex, disputed, or high-value estates |

| Full personal liability for errors | Professional indemnity protection |

| Time-consuming — you manage all paperwork | Solicitor manages all correspondence and HMRC forms |

While DIY saves money in court fees, the risk of errors — which can result in HMRC investigations, personal liability, or delayed distribution — means that professional advice often pays for itself.

NPS Law’s probate solicitors offer a free initial consultation. Contact us today to discuss your situation and get a clear, fixed-fee quote.

The main costs involved in the probate process are:

For a detailed breakdown of all costs, see our guide: How Much Does Probate Cost in the UK? Solicitor Fees Explained.

You can market a property and accept an offer before probate is granted, but you cannot legally complete the sale until the Grant of Probate (or Letters of Administration) has been issued. For more detail, see our guide: Can You Sell a House Before Probate Is Granted in the UK?

If the deceased did not leave a valid will, the estate is distributed according to the Rules of Intestacy. A close relative applies for Letters of Administration using form PA1A. The order of priority for intestacy is: spouse or civil partner first, then children, then parents, then siblings. If you are unsure how intestacy rules apply to your situation, a solicitor can advise.

Yes. A will can be challenged on grounds including lack of testamentary capacity, undue influence, or improper execution. A claim for financial provision can also be made under the Inheritance (Provision for Family and Dependants) Act 1975. Contested probate can significantly extend the administration timeline and should always be handled by a specialist solicitor.

Once the Grant of Probate is issued, you can begin collecting assets, paying debts, and ultimately distributing the estate. For a full guide to this stage, see: Once Probate Has Been Granted, What Happens Next?

Scotland has a different legal system. The equivalent process is called Confirmation, and the document granted is a Certificate of Confirmation rather than a Grant of Probate. This guide covers England and Wales only.

The probate process in the UK involves several distinct stages — from registering the death and valuing the estate, through to applying for the Grant of Probate and distributing assets to beneficiaries. For a straightforward estate, the process typically takes between six and twelve months from start to finish.

If the estate is complex, involves property, or if you are concerned about inheritance tax or potential disputes, taking professional legal advice early can save significant time, cost, and stress.

NPS Law’s probate solicitors are experienced in all aspects of estate administration. Contact us for a free initial consultation — we offer clear, fixed-fee probate services with no hidden costs.

©️ Copyright 2026 NPS Law is a trading name for NPS Law LLP. Solicitors of England and Wales. Authorised and Regulated by the Solicitors Regulation Authority. SRA Number 570169. A list of all Partners is available on the SRA directory for this firm. website designed by origin-media